Analyzing Practical Implications of Most Economically Advantageous Tender (MEAT)

June 2, 2022

Leadership Styles Practiced by Manager in LCCA

June 2, 2022

Critically Evaluation

Download PDF File

Download PDF File

This study zooms in on how the Ice Department handles its money and plans its finances. It's like taking a close look at how they manage their budget to keep things cool and efficient. The evaluation of accounting, particularly management accounting, is pivotal as one of the primary drivers shaping the entire organization. This accounting system is also valuable for different organizational departments' performance assessments. Additionally, these departments facilitate data-driven decision-making based on performance metrics for the organization's management and ethical considerations in an organisation. In contrast, traditional financial accounting possesses distinct characteristics that prove advantageous to the company's shareholders, as Smith (2017) highlighted. It strives to give the company's management insights that enable them to provide feedback to the marketplace effectively. This, in turn, allows the company to gauge its financial performance relative to competitors and industry standards.

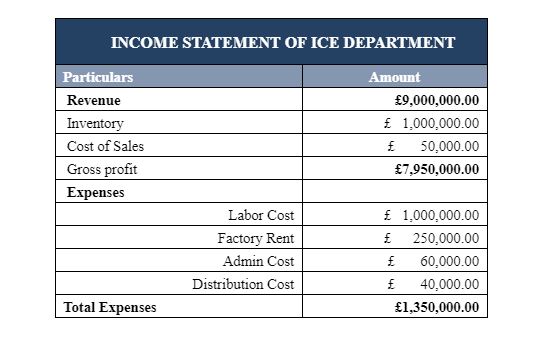

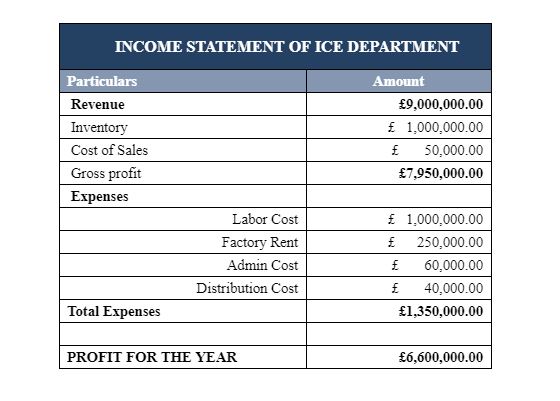

Income Statement

The income statement for the Ice Department primarily consists of various categories, focusing on revenue or sales generated by the company, costs associated with sales, and various company expenses. Among these categories, distribution cost plays a crucial role. The income statement, prepared in accordance with IFRS standards, provides a comprehensive overview of the company's annual profit. This statement includes detailed information on distribution costs and other key components such as factory rent, administrative expenses, and labour costs.

Break-Even Analysis

A break-even analysis has been performed to calculate the Ice Department's safety margin. From the managerial accounting perspective, the company's break-even analysis differs slightly from financial accounting. Factors of revenue and profits are different in both aspects of accounting. Products can be made more costly to generate more revenue. The main variables for the calculation of the break-even analysis of the Ice Department are total variable cost comprised of labour cost on the product and fixed cost consisting of expenses.

Review Strategic Analysis of LEGO

From the above analysis of the Ice Department, 1944 units are calculated as the break-even point, which means at this point, the Ice Department has zero loss and zero profit. However, the Ice Department desired to make a profit of $100,000 for a specific period, and for this purpose, it sold at least 2,500 units.

Conclusion

The exploration of management accounting dissertation topics presented in the assignment underscores the significance of managerial accounting as a vital instrument employed within organizations to assess the performance of diverse departments. Conversely, accounting and finance in an organisation operate from a contrasting standpoint. However, it's noteworthy that the Ice Department's job cost system delves into the comprehensive analysis of the company's costs incurred by the management from various angles.

Assignment Part 2

In the following assignment, different tools are considered for the budgetary control of the Ice Department Company.

Introduction

Planning tools are essential for effective budgetary control in any organization. These tools serve as the compass, guiding financial decision-making and ensuring fiscal responsibility.

A few financial problems have been highlighted for the Ice Department, and it's one of the Competitors in the United Kingdom (i.e. Klarstein Company). These problems are Brexit, efficiency, and maximizing profitability. Lastly, these problems are being solved in the light of management accounting.

Planning Tools for Budgetary Control

The main role of managers of the company is to make decisions based on the information provided by the project manager accountants. These decisions are mostly related to planning and forecasting the sales and profit of the company in many aspects. In this way, different goals of the company are achieved with the help of their decisions (Garrison et al., 2010; McLellan and Moustafa, 2011). These tools help the company's management allocate resources to increase productivity and save time.

Impact of Corporate Governance on Financial Performance of SMEs in Nairobi's Retail Industry

On the other hand, companies use different types of planning tools. Regarding the Ice Department, budgetary control is based on future information. Moreover, the company estimates future needs (i.e. financial) in an order based on budgetary control. Another purpose of this control system is to control the company's financial performance.

Responding to Financial Problems

Financial and management accounting is regarded as essential for the organization as it has the capacity to change the financial performance of the company and its financial position through financial analysis. Following are some financial problems for the Ice Department Company.

1. Brexit

Brexit is regarded as one of the main unusual problems for all companies in the United Kingdom. Several factors associated with Brexit create problems for companies. For example, there is uncertainty that if the United Kingdom leaves the European Union, it may be unable to do so. In both aspects, it will have some positive impacts on the financial performance of the companies as well as negative impacts. In terms of the Ice Department, it can be a problem related to the labour and production of the company.

2. Efficiency

The Ice Department Company is based on several departments. Therefore, the performance of each department is essential for the company's performance. Efficiency is one of the other problems associated with the company's financial performance.

3. Maximizing the Profitability

The financial position of the Ice Department Company is sometimes measured for a specific period from its profitability. In this way, it is compared with its competitor, Klarstein Company. Maximizing the company's profitability is also related to the company's financial problems in management accounting.

Review Analytic Study of Pandemic and Financial Crises- A Recommendation for LAFICO

4. Ice Department as Respondent

As mentioned above, the Ice Department faces problems in terms of financials. Therefore, these problems must be sorted out to increase the company's productivity. To solve these problems, the Ice Department Company's operational management reduces the costs associated with the operations, like the distribution of the products. The company can also reduce the quantity of the product in inventory. The company's management can also reduce the other expenditures and price of the product to increase sales, ultimately positively affecting the Ice Department's sales.

5. Klarstein Company as Respondent

Klarstein Company is another company that is also into ice making by its profile and is also regarded as a competitor of the ice Department. This company is also facing these above-mentioned financial problems, and the management of the Klarstein Company has taken certain steps to mitigate these problems. The company has evaluated the performance of each department with the help of management accounting to find a specific department that needs to be focused more. Moreover, most of the costs associated with different operations have been reduced with the help of management accounting.....

If you want to access the complete assignment above, message us on WhatsApp or by Email. We will get back to you within 24 hours.

References

Drury, C. (2015) Management and Cost Accounting. 9th Ed. Cengage Learning.

Edmonds, T. and Olds, P. (2013) Fundamental Managerial Accounting Concepts. 7th Ed. Maidenhead: McGraw-Hill.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial accounting. Issues in Accounting Education, 25(4), pp.792-793.

Gupta, A., 2013. Environment & PEST analysis: an approach to the external business environment. International Journal of Modern Social Sciences, 2(1), pp.34-43.

Halik, J., 2012. The application of PEST analysis based on EBRD and IBRD methodology. Central European Business Review, 1(3), pp.14-21.

Horngren C, Sunden G., Stratton, W., Burgstalher, D. and Schatzerg, J. (2013) Introduction to Management Accounting. Global Ed. Harlow: Pearson. (This text is available electronically and is supported by access to an online course.)

McLellan, J.D. and Moustafa, E., 2011. Management accounting practices in the Gulf cooperative countries. International Journal for Business, Accounting and Finance, 6(1).

Mehrdad, 2015. The Role of Management Accounting in the Organization [Online] Available at: [https://pdfs.semanticscholar.org/a342/c6bff164ea4c36013506e4e1e29b02ba07d9.pdf] [Accessed on 4 February 2020]

Saeed, 2015. The Role of Management Accounting in the Organization [Online] Available at: [https://pdfs.semanticscholar.org/a342/c6bff164ea4c36013506e4e1e29b02ba07d9.pdf] [Accessed on 4 February 2020]

Seal, W. et al. (2014) Management Accounting. 5th Ed. Maidenhead: McGraw-Hill.

Shushila, 2019. Management Accounting: Meaning, Nature, Characteristics, Objectives, Tools, Advantages and Limitations [Online] Available at: [ http://www.accountingnotes.net/management-accounting/management-accounting-meaning-nature-characteristics-objectives-tools-advantages-and-limitations/17041] [Accessed on 4 February 2020]

Smith, S.S., 2017. Integrated Financial Reporting & Management Accounting An Opportunity for Strategic Leadership. Journal of Business & Economic Policy, 4(1).

Ward, K., 2012. Strategic management accounting. Routledge.

Get 3+ Free Dissertation Topics within 24 hours?