Comparative Assessment of European and Chinese Civil Engineering Standards

December 20, 2020

Prospects of Enhancing Global Economy Through International Trade Liberalization

December 20, 2020

Consultancy projects are the lifeblood of many businesses today. Whether you're a seasoned consulting firm, a small business owner looking for expert guidance, or an individual seeking specialized advice, consultancy projects are pivotal in driving growth, solving complex problems, and achieving specific objectives. In this blog, we'll explore the fascinating world of consultancy projects, uncovering the key elements, best practices, and success stories that make them essential to modern business.

Explore More About Consultancy Project in International Business

A consultancy project is a collaborative engagement between a consultant or consulting firm and a client to deliver expert advice, solve problems, or provide solutions. These projects typically have a well-defined scope, a specific objective, and a finite timeline. They can cover various domains, such as management, technology, marketing, finance, etc. Whether you're a consultant looking to enhance your skills or a client seeking expert guidance, understanding the art of a consultancy project is essential for achieving your goals in today's complex business landscape.

Executive Summary

The consultancy project's primary objective is to explore and assess four alternative asset classes as viable investment options. This consultancy aims to empower investors with valuable insights into emerging asset classes, including precious metals, collectable cars, wines, and art/antiques. Additionally, it seeks to offer recommendations on integrating these alternative assets with traditional ones, such as stocks and bonds, while providing a comprehensive overview of the associated risks.

Research for this project involved a combination of secondary literature obtained from the university library, internet-based research, and database searches. It also included primary data collection through semi-structured interviews with fifteen investment fund managers in the South East England region. It was selected via purposive sampling to tap into professionals' expertise in alternative asset classes.

The research findings indicate that these four alternative asset classes can be viable investments, offering attractive returns when approached with appropriate diversification strategies to mitigate risk. This consultancy project provides practical recommendations to guide investors in allocating and diversifying their portfolios to tap into the profitability of these alternative asset classes.

Background

While alternative investments were once considered exclusive to high-net-worth individuals and sophisticated organizations, they have become increasingly mainstream. Innovations have made alternative investments accessible to a wider range of investors, offering various strategies and geographic regions to explore (Blessings, 2011). Alternative assets encompass diverse investment methods, including physical assets like real estate and natural resources, and alternative approaches such as private equity (Conovor et al., 2007). When selecting individual assets, these investments often depend on innovative strategies or specific knowledge (Campbell, 2005).

The primary advantage of alternative assets is their lower correlation with traditional investments, potentially enhancing portfolio returns and stability (Skidmore, 2010). This consultancy project seeks to analyze four alternative asset classes—art and antiques, wines, collectable cars, and precious metals—compared to traditional stocks and bonds, providing insight into the risks and returns associated with these alternatives.

Objectives of Consultation

The objectives of this consultancy project are as follows:

Evaluate the effectiveness of traditional asset classes for strategic asset allocation in the contemporary global business environment.

Assess the efficiency and potential of alternative asset classes, specifically art and antiques, collectable cars, wines, and precious metals, for diversification and risk management in investment portfolios.

Understand the systemic risks and correlations between the recommended alternative asset classes as investment options for contemporary investors.

Ultimately, this consultancy project aims to equip contemporary investors with the knowledge and recommendations to effectively explore rapidly emerging asset classes.

Industry Background

Today, asset managers are exploring alternative asset classes to seek higher yields in a low-interest-rate environment, a trend expected to persist. Investors turn to alternative investments to achieve higher, uncorrelated returns in a low-return environment. Historically, alternative investments were primarily accessible to institutional or high-net-worth investors due to their complexity (Anderson, 1974).

A World Wealth Report from 2002 revealed that high-net-worth individuals (HNWIs) had approximately 10% of their financial assets invested in alternative assets, including structured products, luxury valuables, collectables, hedge funds, managed funds, and precious metals (Merrill Lynch and Cap Gemini Ernst & Young, 2003). Although this share slightly decreased to 9% by 2007, the interest in alternative assets among HNWIs remained significant.

Over the last decade, institutional interest in alternative asset classes has grown, driven by market events such as the equity market downturn 2000 and the low-yield bond environment. This shift prompted investors to allocate a substantial portion of their assets away from traditional investments and into alternative asset classes (Hubbard and Waltz, 2010). An estimated $200 billion flowed into alternative assets in 2005 (Russell Investment Group, 2005), with predictions indicating that alternative investments would continue to gain momentum.

This consultancy project aims to shed light on these evolving trends in alternative investments, providing investors with insights into four specific alternative asset classes and their potential for portfolio diversification and risk management.

Consultancy Process

The consultancy process is a structured and systematic approach to providing expert guidance and solutions to clients. It typically involves several key stages, including understanding the client's needs, data analysis, strategy development, implementation, and ongoing support. Effective communication, collaboration, and a commitment to ethical standards are essential throughout the process to ensure success and client satisfaction. The consultancy process is a roadmap for consultants to deliver value and help clients achieve their objectives, making it a cornerstone of modern business advisory services.

Research Methods

As proposed, the current project used interpretive and inductive research approaches. The interpretivism approach allows researchers to interpret elements of the study, thus allowing human interest in the study. Based on this research philosophy, the position of meaning-making practices of human subjects is the focal point of the scientific explanation (Bevir et al. 2008). It is generally termed qualitative research and is conducted from an experience-near perspective. The researcher does not begin with concepts determined before the research but instead looks to have them emerge from experiences revealed through research in the field (Klotz et al., 2007).

The interpretive approach relies greatly on natural methods, including interviewing, observation and analysis of the text. This is evident in the current project as the researchers used the methods of semi-structured questions posed to investment fund managers in the South East of England. The latter considers alternative asset classes viable investments, particularly wines, collectable cars, art/antiques, and precious metals. Using this philosophy, the researcher ensured adequate dialogue between the researcher and the interviewees to construct a meaningful reality collaboratively. Angen (2000) asserted that evaluating research from an interpretive perspective means carefully considering and articulating the research question and having ethical and substantive validity.

Furthermore, the inductive research approach was essential to the current consultancy project. It was required to explore the topic from specific observations to broader generalisations and theories to comprehend the investment feasibility of alternative asset classes. The inductive approach is often called the “bottom-up” approach, as the researcher moves from observation, pattern, and tentative hypothesis to theory. This was the most suitable design for the current research as the consultancy project seeks to comprehend the use of alternative asset classes in the contemporary business environment. The strategy used to develop research methods was suitable for secondary data sources.

Sample Design

The semi-structured interviews were conducted using fifteen (n=15) participants who were investment fund managers. To choose the participants, a purposive sampling technique was used. Specific requirements were set to obtain individuals to be sampled, such as specialist knowledge in alternative asset classes, specifically wines, collectable cars, arts/antiques, and precious metals. Other criteria included capacity and willingness to participate in the research. Specifically, the type of purposive sampling technique used was expert sampling, as the current study needed to be enriched with knowledge that only individuals with specific expertise can provide. Participants were selected from the South East of England locality, including Berkshire, Buckinghamshire, East Sussex, Hampshire, Kent, Oxfordshire, Surrey, and West Sussex. A quick search on the internet provided a list of investment fund managers within these areas.

Once a comprehensive list was composed, participants were eliminated based on their expertise, and those with experience and expertise in alternative asset classes were considered. Further elimination of data occurred when investment fund managers were contacted. First contact was made through e-mail, in which an introduction of the researcher and the consultancy project were introduced and through telephone. After this, fifteen investment fund managers agreed to provide the interview.

Review of Secondary Data

Secondary data was obtained from the university library and through database searches on the internet and the university library database. Academic peer-reviewed literature was searched from databases focused on alternative asset classes. It is noted that a majority of the literature found did not refer specifically to the asset classes of choice (i.e. arts/antiques, collectable cars, wines, and precious metals). This is because these specific four classes have been emerging recently as an investment choice for individual investors who are not considered institutional investors or HNWIs. Empirical data was also considered for this consultancy report, even though it is a qualitative research paper to understand the profitability and risks associated with these alternative investment choices compared to the traditional asset class.

Results of Consultancy

Alternative investments are commonly used to reduce overall investment risk through diversification. Often, alternative investments carry the characteristics of being (as cited in Burton and Jacobsen 2001; Campbell 2005; Conovor et al. 2007; Eling and Marek 2011; Fassas 2012);

- Low in correlation to stocks and bonds, the traditional financial investment options

- It is difficult to determine the current market value

- Are considered relatively liquid

- Relatively high cost of purchase and sale

- Limited historical risk and return data on asset

- Often, it may require a high degree of investment analysis before the actual purchase takes place

Based on a review of the literature and data acquired from investment fund managers, the four alternative asset classes could offer three potential advantages to an investment portfolio: diversification, higher return potential, and access to innovative investment strategies. The advantages obtained from investing in art/antiques, collectable cars, wines, and precious metals are explained as follows;

- Diversification: Generally, alternative investments have a low correlation to public stocks and bond markets. This means that price movements in publicly traded stocks and bonds will usually not parallel alternative investments Hubbard and Waltz 2010. This provides the potential to develop a strong portfolio using alternative investments as diversifiers. It is evident and usually found that when a publicly traded investment is producing a trend of steady decline, there is a great possibility that the investment in an alternative asset class, particularly precious metals, may gain or hold a trend that is categorised as steady (Mamarbachi et al. n.d; Hubbard and Waltz 2010).

- Higher return potential: the research found that alternative investments have the ability to balance investment returns within an individual’s portfolio (Worthington and Higgs 2004). Most investment fund managers have reiterated that it is common to find that when a traditional investment, such as a stock or bond, is underperforming, the alternative investment may be gaining or holding a steady position (Masset and Wiesskopf 2010).

- Innovative investment strategies: it was found in the study that investment fund managers frequently use innovative strategies for alternative investment to manage risk and pursue more significant returns, which are not commonly used in traditional investments (Hubbard and Waltz 2010). Some of the strategies used for investment by the managers that had overlapped from data collected in interviews for wines, collectable cars, arts/antiques, and precious metals have been leverage, arbitrage, short selling, derivatives, and futures (Andrews and Benzing, 2007).

It is reiterated that diversification does not always assure profit or loss. Instead, alternative investments cover a diverse range of categories, styles, and philosophies, which are different for each investment fund manager responsible for running them. Even though it was found that investment managers differed in their individual risk and return characteristics, they shared common characteristics that overlapped within the alternative asset class investments.

One of the most important aspects discovered is using alternative asset classes to spread risk. When diversifying into other asset classes, the investor can spread the risk as there are more places in which an investment is placed, and there is a decreased chance that the overall portfolio will be damaged in case a single asset class slumps. The alternative assets of wines, arts/antiques, and collectable cars have an added physical value. These assets have an intrinsic worth above and beyond their investment value. Blessings (2011) states alternative asset classes perform exceptionally well when hedging against inflation. Campbell (2005): Conover et al. (2007), and BlackRock (2011) affirms that when inflation occurs, the currency can buy less of a given basket of goods, but if an individual is the owner of these good, there is more of monetary value for each of them. Investment fund managers confirmed that during inflation, the asset class of precious metals and collectables tend to increase in value and recommend investing some funds into these (Black Rock 2010). There are also added lifestyle benefits associated with alternative asset classes. Investment fund managers state that investing in art, antiques, and other collectables, such as cars and wines, can be an enjoyable hobby besides diversifying the investor’s portfolio (Blessings 2011). There is also the probability that many of the investing expenses can be deducted if they are itemised, allowing the investor to strain extra savings from the cost of acquiring these alternative assets.

The four alternative asset classes were further scrutinised using tools such as the PESTLE analysis, SWOT analysis, and Risk Review Framework. Understanding the risks and challenges associated with alternative asset class investment is critical to making more informed decisions towards the investment. Often, investors seek to operate in complex, competitive, and global markets that vary in products and asset classes. This brings exposure to the uncertainty viewed as a risk and categorised into systematic or non-systematic risks. According to Blessings (2011), systematic risks entail the challenges created by the unpredictability and volatility of the market. Andrews and Benzing (2007) state that at times of high valuations, it is recommended to exit an investment at favourable prices and obtain a good return as it is the easier route. However, at times of low valuations and depressions in a market, it becomes difficult to exit the investments made for good returns. Still, the circumstances bring about various opportunities for investing in attractive valuations. Non-systematic risks apply to only specific investments, contrasting the above and affecting the entire market. Markowitz (1952) confirms that this can be eliminated through adequate diversification within asset classes.

| Risk Review Framework | |||

| Risk Type | Score (0-10) | Applicable Risk | Mitigation Strategy |

| Market Risk | 5 | Interest Rate/Currency Risk | When considering investments that need currency and interest rate swaps, professional advice and arbitrage knowledge are needed. |

| Credit Risk | 9 | Transaction Risk | Each alt. investment holds its own transaction risk. Mitigation will include detailed due diligence and ongoing reporting. |

| 6 | Portfolio Concentration | Moreover, the concentration of investment funds towards one asset or industry must be avoided and controlled. | |

| Operational Risk | 5 | Operations | Investor fund manager compliance and security are to be managed by investors to ensure discrepancies. |

| Regulatory Risk | 9 | Governance | All alt. investment considerations need to consider applicable governance rules |

| 9 | ESG* | Alt. Investment considerations need to take into account the ESG framework and rules. | |

| Counterparty Risk | 7 | Investment Exit | Seeking an investment partner that has the ability to handle counterparty through negotiation, management, and diversification. |

Table 1- Risk Review Framework for Four Alternative Asset Classes

In addition to the risks outlined above, it is essential that investors consider other risks associated with investing in the four alternative asset classes. Below is a PESTLE review identified as associated with the four assets found in literature and through interviewing investment fund managers (Blessings 2011).

| Factor | Description | Impact on Investment Strategy (Opportunity or Threat) |

| Political/Legal | · Foreign trade regulations · Stability of government · Terrorism/Crime Issues | · Threat · Threat · Threat |

| Economic | · GDP decrease · Inflation instability · FDI decrease · Cost of living · Increasing cost of goods | · Opportunity · Opportunity · Threat · Threat · Threat |

| Socio-cultural | · Lifestyle changes | · Threat |

| Technological/Infrastructure | · New tech development, emerging trends · New products | · Opportunity · Opportunity |

| Ecological | · Environmental protection laws · Sustainability Awareness · Environmental protectionism | · Threat · Threat · Threat |

Table 2- PESTLE Analysis of Four Alternative Asset Classes

It is essential for the investor to understand existing and perceived challenges when investing funds in the four alternative asset classes. Each point has been rated using a scale of 1-10, with 1 = weak and 10 = strong.

| Threats | Rating 0=Low 10= High |

| Competitors | 6 |

| Economic slump | 5 |

| Changing global environment | 4 |

| Credit crunch/downgrade | 5 |

| Stronger regulation | 3 |

| Higher taxes | 3 |

| Opportunities | |

| Niche investment market | 10 |

| Strong selling point | 8 |

| Unique business model | 10 |

| Strengths | |

| Innovative service solution | 10 |

| Diversification of portfolio | 8 |

| Association with strong brand | 7 |

| Weaknesses | |

| Poor investment choices | 9 |

| Cash flow | 5 |

| New to the market unknown territory (sustainability investment) | 8 |

Table 3- SWOT Analysis of Four Alternative Asset Classes

The above risk review framework, PESTLE, and SWOT analysis identified the perceived risks of the four alternative asset classes. It shows that the risks and challenges associated with such investment classes are real, but the associated risks can be mitigated using a realistic approach.

Recommendations

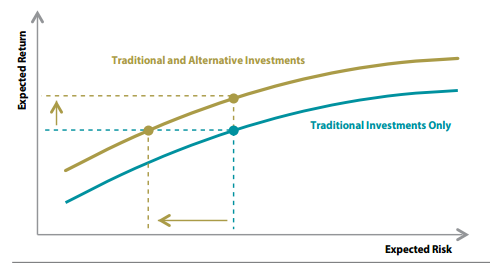

Notwithstanding the unique risks involved in alternative investments, they are considered a useful tool for improving the risk-return aspects of an investment portfolio. As mentioned, they have the ability to increase diversification, reduce volatility, give low correlations to traditional investments and offer the end-user enhanced returns because there is a broader investment opportunity. The graph below illustrates a Markowitz efficient frontier by representing low-risk portfolios that have been measured using volatility as a factor for a given return. It is evident that including the four alternative asset investments results in the efficient frontier moving up and to the left (Baird Private Wealth Management 2013). Thus, for a given level of return, the risk is lower or vice versa. With a given level of risk, the returns are higher.

Figure 1- Markowitz Efficient Frontier (Source; Baird Private Wealth Management, 2013)

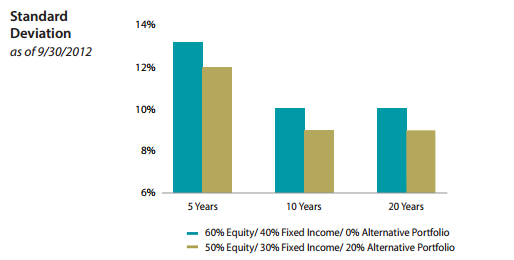

Alternative investments, when on their own, can have higher volatility than traditional asset classes, specifically fixed-income ones. However, alternative investments have low correlations to more traditional asset classes, which can be useful in economic slumps or portfolio diversification (Blessings 2011). It is recommended that investors include some of the four alternative asset classes in their portfolios as it tends to result in lower overall volatility, which is evident in the graph below.

Figure 2- Standard Deviation and Diversification of Alt. Asset Classes (Source; Baird Private Wealth Management, 2013)

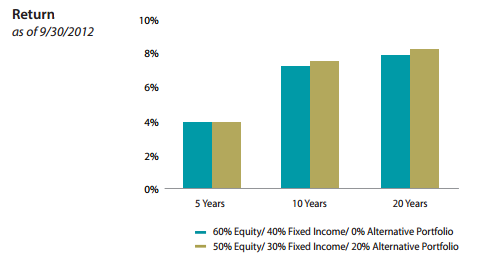

Investors can also take advantage of having a potential for higher long-term performance than their traditional asset counterparts because they have a wider market in which to invest, which includes both public and private, but are known not to have similar investment constraints (Blessings 2011). This is evident in the graph below.

Figure 3- Returns on Alt. Asset Classes (Source; Baird Private Wealth Management, 2013)

There are risks involved with such investments, including (Burton and Jacobsen 2001; Campbell 2005; Conovor et al. 2007; Eling and Marek 2011; Fassas 2012);

- Higher fees

- Greater complications

- Less transparency

- Less Liquid

- Less tax-friendly

- May not have the ability to diversify risk in an extremely down market

Therefore, it is recommended to mix the investor’s portfolio with both traditional and alternative asset classes to ensure the soundness of the portfolio and the use of investor funds. Four main deliberations must be considered before incorporating the four alternative asset classes into the portfolio.

- Investors should take a more conservative approach with these investments by electing specific strategies with a proven track record, stable investment team, and existing processes (Black Rock 2010). New products will be offered regularly as it is a fast-growing market, making it recommended to exercise caution and place a bias for offerings that have demonstrated themselves through success instead of back-tested track records.

- It is recommended to allocate 10-20 per cent of a portfolio to alternative investments. This is considered large enough to be impactful for producing returns and reducing risk. At the same time, it is not so large that it dominates the portfolio as a whole (Blessings 2011).

- Each analysed alternative asset has different objectives and should be funded differently within the portfolio. Alternative investments that enhance returns and reduce volatility need to be proportionately financed from the investment portfolio (Black Rock 2011).

- To successfully incorporate alternative investments into a portfolio, it is necessary to determine the most appropriate structure that is not just based on net worth levels but also considers liquidity needs and overall risk objectives and return objectives (Blessings 2011).

Conclusion

Traditional asset classes such as stocks and bonds have dominated investment historically. However, alternative asset classes have rapidly become the investment choice for many. Traditional asset classes such as stocks and bonds have been efficient for investment, producing returns through a predictable investment strategy. According to Skidmore (2010), institutional and individual investors have begun to explore alternative assets to increase returns and diversify risk. Since globalisation has greatly impacted the global economy, traditional assets such as stocks and bonds have become progressively linked. As seen in many cases, alternative assets’ performance is usually highly dependent on the characteristics of the individual investment rather than being positively correlated to the market at large. In precious metals, the asset class tends to behave very differently from stocks and bonds.

Various kinds of benefits come from investing in alternative asset classes. To construct a good portfolio, it is essential to diversify investments so that if one type of investment is performing poorly, another is doing well.

Alternative investments attempt to accomplish their returns by using unique investing strategies rather than activity from the market to exploit market ineptitudes which the market has yet to identify. This results in an added layer of diversification that can complement more traditional asset classes. It should be noted that diversification alone can’t guarantee a profit or ensure against loss. Furthermore, the unique properties of alternative assets mean that they come with a high degree of risk but also offer the potential for returns that may not be correlated with other markets. Aside from investment value, alternative investments such as art/antiques, collectable cars, wines, and precious metals are a simple pleasure to own.

References

Anderson, R. C. (1974) “Paintings as an investment.” Economic Inquiry

Andrews, T., and Benzing, C. (2007). The determinants of price in internet auctions of used cars.” Atlantic Economic Journal

Angen, M. J. (2000). Evaluating interpretive inquiry: Reviewing the validity debate and opening the dialogue. Qualitative Health Research.

Baird Private Wealth Management. (2013). The roles of alternative investments in a diversified investment portfolio. BAIRD. [online] Available from < https://www.rwbaird.com/bolimages/Media/PDF/Whitepapers/Demystifying-the-Role.pdf>. [Accessed: 7th December 2015].

Burton, B. J., and Jacobsen, J. P. (2001). The rate of return on investment in wine.” Economic Inquiry.

Bevir, M. and Kedar, A. (2008). Concept formation in political science: An anti-naturalist critique of qualitative methodology. Perspectives on Politics

BlackRock (2010). Alternative investments: Risk analysed.” BlackRock Solutions. [online] Available from < https://www2.blackrock.com/content/groups/uksite/documents/literature/1111145534.pdf>. [Accessed: 5th December 2015].

BlackRock. (2011). Protecting against alternative investment risk. BlackRock Solutions. [online] Available from < http://www.blackrock.com/corporate/en-emea/document/documents/web/corporate/newworld/institutional/protect-against-alternative-investment-risk.pdf>. [Accessed: 5th December 2015].

Blessing, S. (2011). Alternative Alternatives: Risk, Returns, and Investment Strategy. Wiley Finance.

Campbell, R. A. J., (2005). Art as a financial investment. The Journal of Alternative Investments.

Conover, C. M., Johnson, R. R., Mercer, J. M. (2007). Can precious metals make your portfolio shine?” CFA Institute. [online] Available from < https://www.cfainstitute.org/about/press/release/Documents/precious_metals.pdf>. [Accessed: 5th December 2015].

Eling, M. and Marek, S. (2011). Corporate governance and risk-taking: Evidence from the UK and German insurance markets.” Working Papers on Risk Management and Insurance, No. 103. [online] Available from < http://www.unisg.ch/~/media/internet/content/dateien/instituteundcenters/ivw/wps/wp103.pdf>. [Accessed: 5th December 2015].

Fassas, A. P. (2012). Exchange-traded products investing and precious metal prices. Journal of Derivatives & Hedge Funds.

Fogarty, J. (2007) “Rethinking wine investment in the UK and Australia.” American Association of Wine Economists. AAWE Working Paper No. 6.

Hubbard, C. M., and Waltz, D. T. (2010). Precious metals and retirement portfolio survival rates. Journal of Business & Economics Research

Klotz, A., and Lynch, C. (2007) Strategies for Research in Constructivist International Relations. Armonk, NY: M. E. Sharpe.

Mamarbachi, R., Day, M., and Favato, G. (n.d.) “Evaluating art as an alternative investment asset.” Capco Institute Journal of Financial Transformation. [online] Available from < http://s3.amazonaws.com/publicationslist.org/data/g.favato/ref-58/09_Evaluating%20art%20as%20an%20alternative%20investment%20asset.pdf>. [Accessed 4th December 2015].

Markowitz, H. (1952). Portfolio selection: Efficient diversification of investments. The Journal of Finance.

Masset, P. and Wiesskopf, J. P. (2010). Raise your glass: wine investment and the financial crisis.” American Association of Wine Economists. AAWE Working Paper, No. 57.

Mercer. (2015). Global insights on ESG in alternative investing.’ Mercer Newsroom. [online’ Available from < http://www.uk.mercer.com/newsroom/global-insights-on-esg-in-alternative-investing-report.html>. [Accessed: 6th December 2015].

Merrill Lynch and CAP Gemini Ernst & Young (2003). World Wealth Report 2003.

Merrill Lynch and CAP Gemini Ernst & Young (2008). World Wealth Report 2008.

Mochnacz, F. (2013). Do precious metals have the capacity to hedge against inflation? Netspar Theses. [online] Available from < http://arno.uvt.nl/show.cgi?fid=133388>. [Accessed: 6th December 2015].

Russell Investment Group. (2005). The 2005-2006 Russell Survey on Alternative Investing.

Topintzi, E., Chin, H., and Hobbs, P. (2007)/ Moving towards a global real estate index: Overcoming barriers.” RREEF Research, Watson Wyatt Global Investment Review.

Worthington, A., and Higgs, H. (2004). Art as an investment: Risk, return and portfolio diversification in major painting markets.” Accounting and Finance

World Economic Forum. (2015). Alternative Investments 2020- An introduction to alternative investments. [online] Available from <http://www3.weforum.org/docs/WEF_Alternative_Investments_2020_An_Introduction_to_AI.pdf> [Accessed 5th December 2015].

Get 3+ Free Dissertation Topics within 24 hours?