Strategic Analysis of LEGO

June 2, 2022

Efficacy of Traditional Methods of Infantile Colic Relief

June 3, 2022

Download PDF File

Download PDF FileThe intertwining of a pandemic and financial crises has been an unprecedented challenge, reshaping the global landscape profoundly. In the wake of the COVID-19 pandemic, financial markets experienced significant turbulence, leading to a widespread reevaluation of risk management strategies and economic policies worldwide. This convergence has highlighted the critical need for organizations and policymakers to understand the complex dynamics between pandemics and financial crises to effectively navigate future uncertainties.

In this blog, we delve into the analytics of pandemics and financial crises, providing recommendations tailored to LAFICO (Libyan Arab Foreign Investment Company) aimed at enhancing resilience and mitigating risks. Understanding the intricate interplay between these crises is essential for LAFICO to adapt and thrive in an environment marked by volatility and uncertainty. By implementing proactive measures and leveraging insights gained from this analytic study, LAFICO can position itself strategically to weather future challenges and capitalize on emerging opportunities in the global investment landscape.

.

Before delving into recommendations for LAFICO amidst the pandemic and financial crises, it is imperative to comprehensively analyze the current economic landscape and the specific challenges it poses.

Introduction

In recent years, the simultaneous occurrence of the COVID-19 pandemic and financial crises has significantly impacted major companies and businesses worldwide. The convergence of pandemics, epidemics, and financial disruptions in the global market has presented a challenge of unprecedented proportions for businesses. Any disturbance in the market triggered by epidemics, pandemics, or financial crises has had adverse effects on businesses, with the ability to measure and calculate losses from financial crises but facing uncertainty when it comes to epidemics and pandemics (Peckham, 2013).

The emergence of pandemics such as COVID-19 has posed a unique challenge due to the difficulty in estimating the extent of potential losses for businesses throughout such events. The presence of a common yet unknown enemy on a global scale, coupled with the lack of prepared vaccines and medicines, makes it challenging for companies to predict and mitigate the impact effectively. While China successfully contained the initial outbreak of COVID-19 in Wuhan, many other countries, particularly developed Western nations like Italy, Spain, and Germany, struggled to control the spread, with the United States initially downplaying the severity of the virus (Sam Wong, 2020; Dan Mangan, 2020).

The highly contagious nature of COVID-19 has prompted over 100 countries to impose restrictions on international travel, leading to disruptions across various industries such as aviation, tourism, and hospitality. Lockdown measures and social distancing protocols have further compounded the challenges faced by businesses, with no clear timeline for resolution until a vaccine is developed, a process that could take at least 18 months or more (Kuznia, 2020).

In light of these unprecedented circumstances, investors and shareholders are understandably apprehensive about the stability of their investments and hesitant to make further commitments to support companies facing potential collapse. Against this backdrop, investors associated with the Libyan Foreign Investment Company (LAFICO), holding an 11% direct and 29% indirect stake in International Hotel Investments PLC (IHI PLC), seek guidance on navigating the current landscape.

To address these concerns, this report aims to examine past epidemics, pandemics, and financial disruptions to assess the potential impact on IHI PLC and explore any opportunities for investors to optimize their investments or mitigate risks amidst the ongoing challenges posed by the COVID-19 pandemic and associated financial crises.

Understanding the historical context of pandemics and financial crises provides valuable insights into their impact on societies and economies, setting the stage for informed analysis and recommendations.

History of Pandemics and Financial Crises

Throughout history, pandemics such as the Black Death in the 14th century, the Spanish flu in 1918, and the HIV/AIDS crisis in the 1980s have profoundly impacted societies worldwide, shaping public health policies and economic landscapes. Similarly, financial crises like the Great Depression of the 1930s, the Dot-com bubble burst in the early 2000s, and the global financial crisis of 2008 have reshaped financial regulations and investment strategies, leaving lasting effects on economies and markets.

Epidemics and Pandemics

To evaluate the co-existence of the COVID-19 pandemic and financial crises, it is essential to highlight an extensive history of pandemics faced worldwide in the past years.

Asian Flu – 1957 to 1958

Asian flu was another pandemic wave of influenza that started in China and claimed the lives of more than 1 million people worldwide. The virus was later found to be associated with the avian flu viruses. The virus rapidly spread, and the first international case was reported in February 1957 in Singapore and later affected Hong Kong and coastal areas of the US in the summer leading to more than 1.1 million deaths worldwide and, alone, 116000 deaths in the US (Jackson, 2009).

Swine Flu - 2009

Swine flu was a new HIN1 strain discovered in Mexico in the spring of 2009. This virus infected 1.4 billion lives worldwide and has been categorized as a pandemic killing nearly half a million people. This virus was contagious among adults and children, and 85% of deaths reported were aged below 65 years, as reported by the CDC. This virus was more unusual than casual flu and seasonal flu, causing death for those over 65 years. However, the older population, mainly those over 65, were immune to the swine flu and were not infected but rarely (Presanis et al., 2009). Meanwhile, today people are also vaccinated for the H1N1 virus and the flu vaccine.

Ebola - 2014

Ebola is a deadly and contagious virus that spread in West Africa from 2014 to 2016, leading to 28600 reported cases and 11325 deaths. The first international case was reported in December 2013, which spread to Liberia and Sierra Leone. These countries were highly affected, but a few cases were reported from the US, Europe, Nigeria, Senegal and Mali (Frieden et al., 2014). Meanwhile, no cure has been found, and it has also been discovered that bats are a source of the Ebola virus that first occurred in Sudan.

Zika Virus - 2015

Zika virus has turned epidemic for several years in Central America and South America since it remained unknown. Later, scientists discovered that it originated from mosquitos and can also be transmitted sexually in humans. However, the Zika virus was found to be harmful to unborn children causing defective births but is not detrimental to children and adults (Campos et al., 2015). Meanwhile, Central America and South America remain a prime location for the virus in humid and warm weather in which mosquitos carry the virus.

Coronavirus (COVID-19) - 2019

Current coronavirus (COVID-19), or nCOV-2019, first emerged in Wuhan, China, in December, infecting 82,431 people and killing 3,322 patients, primarily overaged or those with existing health conditions. Out of this number, 76,571 people have recovered and become immune to the virus, while China also contained the virus to zero (WHO, 2020). However, since the virus was contagious and inappropriate measures of major developed countries led to a worst-case scenario in which Iran and many European countries, America remains an epicentre of the virus due to a high number of cases (Tan, 2020).

As of 2 April 2020, the virus has infected more than a million people in more than 185 countries and caused more than 50,000 deaths (Arcgis, 2020). Meanwhile, no cure has been found, but the data suggests that 85% of people have mild or no symptoms and become immune in 14 days without special treatment. However, the older population, including those with pre-existing health conditions, are vulnerable to viruses. Most deaths have also occurred among the ageing population due to weakening the immune system (Wu and McGoogan, 2020). However, data from China suggests children are entirely immune to the virus.

Financial Crises

Upon relating the COVID-19 pandemic and financial crises, investigating the latter provides a wider view of the scenario.

OPEC – Oil Crises

The oil crisis began in 1973 during the Arab – Israeli conflict; the oil prices were skyrocketing as Arab nations halted oil exports to the United States in retaliation for arms supplies to Israel. The oil shortage led to economic crises in the US and many other developed countries, leading to very high inflation in those countries due to the shortage of oil (Rustow, 1977). Therefore, it affected the entire supply chain system, tourism, and aviation industry. Meanwhile, it took years for those countries to achieve a target level of inflation.

Asian Crises

The Asian crisis took place in 1997 in Thailand and spread to the rest of the countries in East Asia where trading partners of the businesses were operating. The core reason behind the crises was the flow of capital from developed countries to Asia with optimism and overextension of credit which led to too much debt accumulation in those economies (Climent and Meneu, 2003). As a result, a fixed exchange rate of Thailand to the US was abandoned due to a lack of foreign currency resources. The emergence of crises created a panic in the Asian financial markets that led to capital flight in which foreign investors opted out of billions of dollars of investment. The East Asian governments were on the brink of bankruptcy, which could also have led to the meltdown of global financial markets (Johnson et al., 2000). Hence, the International Monetary Fund (IMF) had to step in and offer bailout packages for these governments to avoid a meltdown in global markets.

Global Financial Crises

The global financial crisis is also known as the sub-prime mortgage bond crisis or, more often, the housing bubble; that took place in 2008 and led to global financial crises, and nearly all countries were affected to some extent. Lehman Brothers, one of the largest investment banks, collapsed overnight, many financial institutions were on the brink of collapse, and nearly all stock markets worldwide had crashed (Obstfeld, 2012). Meanwhile, governments of respective countries stepped in to provide bailout packages to avoid further economic losses, and recovery of the market took almost a decade to recover from the crisis. This crisis has been categorized as one of the worst financial crises after the great depression; the core reason is that suddenly millions of jobs were wiped out, and around $2 trillion was measured for the global economy (Claessens et al., 2010).

Global Economic Perspectives

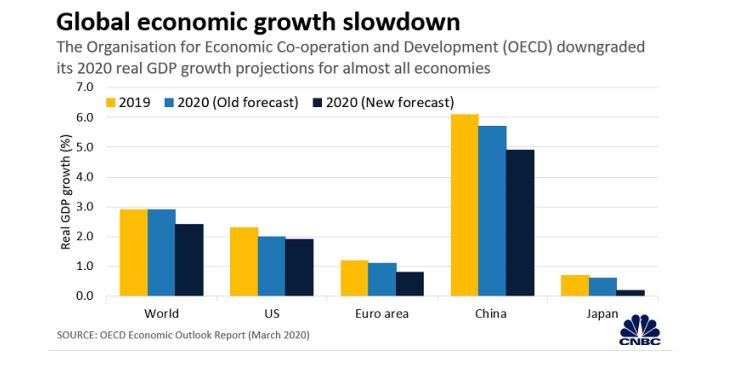

The economic effect of a global pandemic can be observed in terms of loss of economic growth, and Figure 1 demonstrates the economic prospects for 2020, old forecasts and new forecasts amid coronavirus and worldwide lockdowns.

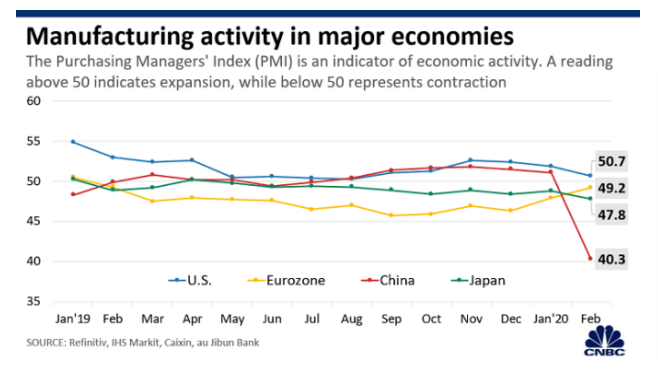

China remains the foremost victim of a downgrade compared to other economies, whereas with the latest numbers, it is expected that China’s economy will grow by 4.9% rather than 5.7% as earlier forecasts (Lora Brown, Palumbo 2020). Similarly, it is also expected that the global economy to grow by 2.4% in 2020 rather than 2.9%, as projected earlier. Figure 2 illustrates changes in manufacturing activities in major economies worldwide.

Figure 2 Manufacturing Activities

China also remains the most affected economy from this pandemic, but China has announced zero-ground virus in Wuhan and has almost contained the virus from China. However, the new cases are travellers around the world, not locals. On the other hand, the US today has become an epicentre of viruses, with cases exceeding 0.2 million and more than 4000 deaths. Hence, this tends to severely affect the US economy and, consequently, worldwide (Lora Brown, Palumbo 2020). Whereas the world’s major countries have locked down countries, small businesses have already halted operations, and travel restrictions have made people wait until their homes. These aspects demonstrate the association between the emergence of the pandemic and the financial crisis initiation.

In addition, the oil prices have reached to record low time after Russia and OPEC failed to reduce production; currently traded at $25 per barrel, as of January 2020, it was at $63.05 per barrel, which means it has lost more than 60% of value. Meanwhile, investors' sentiments have negatively affected the world’s largest stock markets, where the S&P dropped (28.8%), Nikkei (22.2%) DOW Jones (24.1%) (Lora Brown, Palumbo 2020). In addition, around 6.55 million people have filed Jobless claims in the United States, which is 19 times higher than usual, and FTSE 100 experienced a worse week than the last financial crisis in 2008 and the dot-com bubble.

Apart from that, 100 countries have banned international travel restrictions, where half of the European and US populations are under lockdown and virtually the overall world. Hence, the effects of these measures on the economy are inevitable and have significantly affected businesses (Blue Swan Daily, 2019). Since governmental advice and restrictions on gatherings have emptied restaurants, restricted travel has affected the aviation industry along the tourism industry, hospitality industry, and other small businesses have also been affected in the worst way. It was due to their interdependence and the same revenue streams from tourism and business trips.

Aside from the tourism industry, secondary effects of social distancing can be observed in the manufacturing industry, where people are confined and practice social distances to contain the virus. Nevertheless, it has slowed shopping again, affecting billions of small businesses that have halted most production worldwide (Bertha, 2020). In widespread and contagious situations, businesses are less likely to operate when there is no buyer except for the fast-moving consumer goods because people have limited their spending on necessities only due to the loss of jobs and businesses.

Tourism Industry and Hospitality Industry

The global tourism industry has been contributing 10% of the worldwide GDP, and the World Travel and Tourism Council has also warned that due to the COVID-19 pandemic, 50 million jobs could be lost worldwide in the travel and tourism industry. It is also anticipated that Asia will be worst affected by this pandemic, where after the outbreak, the industry could take up to 10 months to recover from the crisis (World Economic Forum, 2020). In addition, the latest strict measures by governments worldwide could be used to anticipate the worst effect on the industry as the US has banned travel to Europe that has halted travel from and in. These measures have also been termed as making the industry in the worst case.

More than 850,000 people travel from Europe to the United States each month, leading to a $3.4 billion loss to the US economy and affecting the tourism and hospitality industry (Skift, 2020). On the other hand, during the pandemic, 50 million jobs will be lost, whereas Asia will have 30 million people jobless related to the tourism and hospitality industry. Therefore, in the wake of travel restrictions, 12%-14% of jobs would be reduced (World Economic Forum, 2020). Thus, the tourism industry is in greater crisis due to pandemics indicating a proportional relationship between pandemic and financial crises for this industry. The effect has also been unquestionably compared to the previous experiences with SARS or H1N1 and the financial crises in 2008. In the current hospitality industry, airlines and cruise operators are hit hard as travel is restricted.

International trips have been cancelled by many organizations around the world, such as Zurich insurer cancelled trips of 2000 employees and others BBVA Deutsche bank have also cancelled the trips of employees to Europe and Asian countries. Similarly, the Chinese Lunar Year has been considered one most prestigious events that attract millions of travellers from around the world to China and enforce airports and the hospitality industry to work at full capacity for months before bookings (Travel Daily News International, 2020). However, due to this pandemic, the Lunar Year celebrations have also been cancelled by the government of China.

To conduct a thorough financial analysis, it is essential to gather comprehensive data and information regarding the company's financial performance and market trends.

Financial Analysis

Financial analysis entails scrutinizing financial statements and market trends to assess a business's health, profitability, liquidity, and solvency, aiding stakeholders in making informed decisions and strategies.

Hypothesis and Assumptions of the Study

- H1: COVID-19 has affected the share price of the company significantly.

- H2: The mean difference between return before COVID-19 and after COVID-19 is equal to Zero

Past Performance

Past performance serves as a critical indicator of a company's historical trajectory, reflecting its ability to navigate challenges, capitalize on opportunities, and deliver results to stakeholders. Analyzing past performance allows for insights into trends, patterns, and areas of strength or weakness, aiding in informed decision-making and strategic planning for the future.

Assets

Figure 3 illustrates the asset performance of the IHI PLC. It can be observed that the company's assets have constantly been growing, indicating its strategy to become highly capital-intensive and diversify and leverage investment geographically to improve revenue streams. Assets in the hospitality industry have been key to success as revenue streams increase, and the value of the assets also rises, which could positively affect the company's financial position.

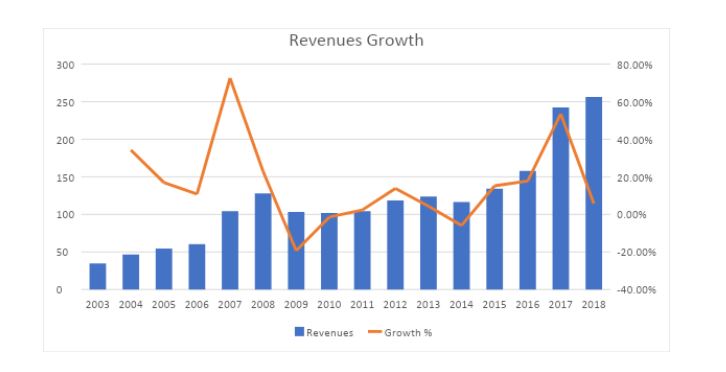

Revenues

Figure 4 demonstrates the revenue streams of the IHI PLC for over a decade. It can be observed that the revenues of the company have been rising but to some extent. On the other hand, negative growth was also observed in 2009 due to the financial crisis. However, the main culprits were lower demand in 2014 and ongoing projects in different continents, including undertaking third-party hotels under management. Critically, lower demand can also be attributed to the Ebola virus in 2014. Similarly, this doubled the revenues and EBITDA of the company till 2017, reflecting the strong revenue growth. Therefore, this implies that IHI has the potential for hard-working, efficient, skilled, and professional employees to handle operations. However, the net profit available to shareholders has not been so attractive over some time; significant fluctuations could be found chiefly downward, as illustrated in Figure 5

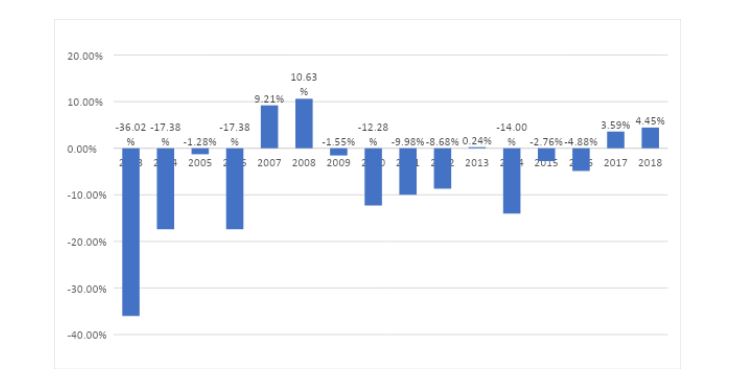

The group experienced an all-time in 2003 with a loss of 36.02%. However, it started to recover in 2007, when it achieved 9.21% growth, followed by 10.63% in 2008 but due to the global financial crisis, then returned to loss until 2016. However, as of 2017 company returned to be profitable till 2018, and potentially 2019, to be reported later. There are two implications from major fluctuations in the company's net profit. One is that the company's assets have been rising consistently throughout the period increasing the taxes and other operational cost burdens for the company; hence it could not arise out of loss almost for 8 years. However, secondly, the company's portfolio increased to its hotels, resorts and other third-party hotels, and commercial plazas started to provide significant profits in 2017, 2018 and 2019. Therefore, based on this assumption, growth in net income was further expected for the year 2020, but the situation remains unclear due to the Coronavirus pandemic, thereby, indicating a correlation between the pandemic and financial crises.

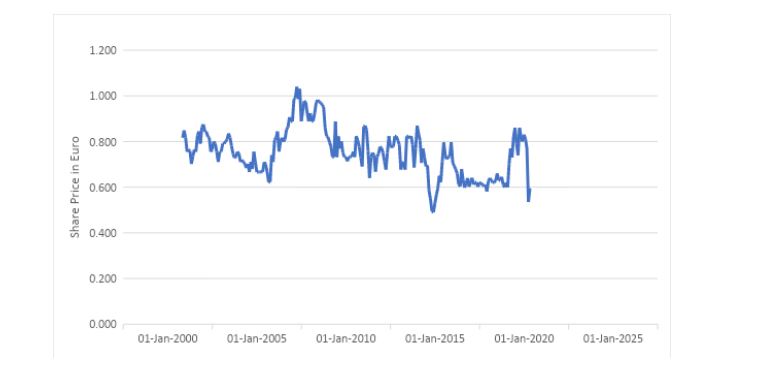

Share Price

The nominal value of the share is €1 per share, but as of 2nd April, the share price was €0.595 has fallen by 28.31% since COVID-19 emerged in December 2019. The graph also shows fluctuations during the period. Meanwhile, changes have been throughout the period since 2000; the average share price has remained at 0.7 to 0.8 since its inception. Therefore, these fluctuations could not be used to measure the company's performance. Instead, fluctuation patterns combined with different time windows could provide valuable insights for investors. For instance, based on the efficient market hypothesis, the market is perfect, and the share price reflects all available market information and is the share's fair and true value.

Therefore, the share price must reflect all the information available in the market in the future. Based on this approach and the assumption, it can be anticipated that IHI PLC has been in the hotel industry for decades and its share prices reflect its performance and the shareholders' value had grown during the financial crises despite reporting a loss for the next 8 years. This implies that the group's survivability is greater than any other company in the market; thus, this performance and strength can be used as a way forward to approach a valuable insight for the shareholders of the company.

Structural Break-Point

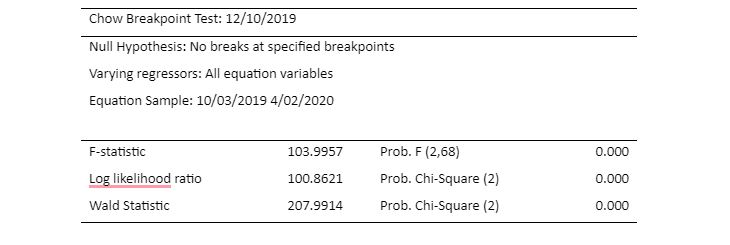

In addition, the Chow breakpoint test has been used to determine if the structural breakpoint at specified data occurs. The core function of the Chow test is to assess the difference between the coefficients before and after the breaking point (Ho and Huang, 2015). A significant difference between the coefficients before and after the scenario is noticeable if the structural breakpoint exists. Meanwhile, the results of the Chow breakpoint are illustrated as follows.

The null hypothesis of the Chow test is that no breakpoints exist at specified breakpoints, and the alternate hypothesis of the test is that there is a breakpoint at specified breakpoints. Since the Prob. F (2,68) is 0.000, which is less than the significance of 0.05; it is evident to reject the null hypothesis of no break points and accept the alternate hypothesis that there is a structural breakpoint at a specified date. Therefore, it could be inferred that the coexistence of the pandemic and financial crises created challenging situations for the company as the emergence of COVID-19 affected the value of shares, resulting in a major challenge that the company might face.

Significance of Difference Mean Return

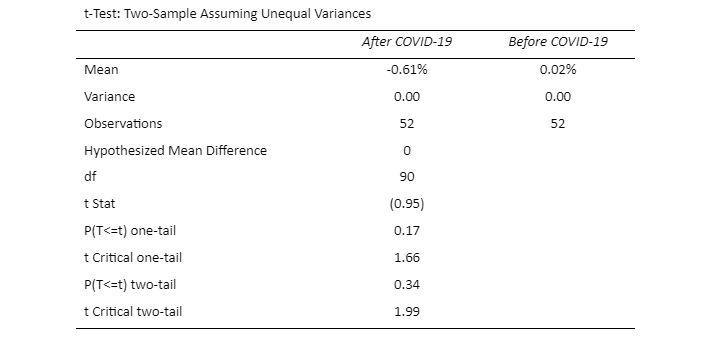

Furthermore, determining the difference between the share price before COVID-19 occurred in December and after the pandemic. In this regard, an independent sample’s t-test has been conducted to determine if the difference between the mean return is statistically significant or not.

The result of the independent sample’s t-test shows that the mean return after COVID-19 was -0.61% is a net loss in value of shareholders, and the average return before COVID-19 was 0.02%, suggesting that shareholders had gained at least 0.02% each day. Upon comparing the average values, it is evident that aside from the existence of difference, it is necessary to determine whether the difference is significant or not. Within the t-test, two-sample assuming unequal variances are observed, whereas the test results suggest that the t-critical value is greater than the t-value.

These values further suggest rejecting the null hypothesis in favour of the alternate hypothesis that states that the difference between the return before COVID-19 and after COVID-19 is not equal to zero. Hence, it is sufficient evidence to argue that COVID-19 has affected the shareholders' returns, which could also place further challenges on the shareholders regarding their investment. The decline in COVID-19 has affected investors’ sentiments. Investors have been opting out of their investments to save the value that shares may lose in upcoming weeks or the foreseeable future.

Future Prospects

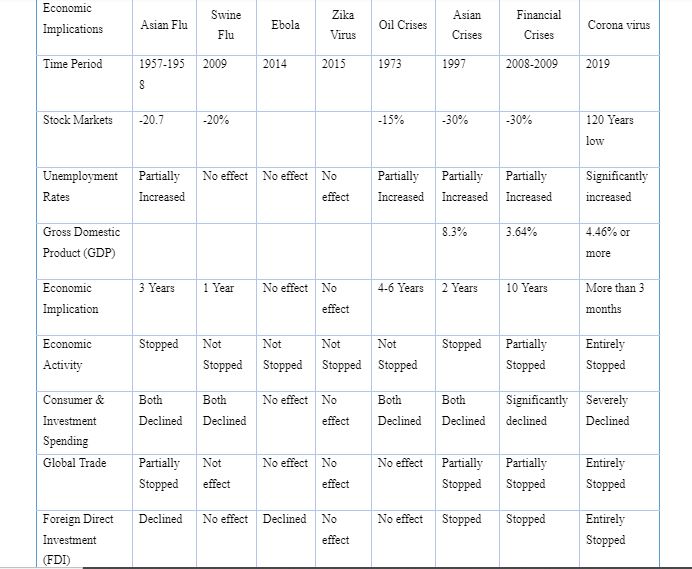

The table above illustrates the similarities and differences between the previous pandemics and financial crises with COVID-19; the data was extracted from multiple sources, and the severity of COVID-19 is different, and there are no similarities between the events. Therefore, we can infer that COVID-19 affects the global economy and tourism industry differently. Meanwhile, stock market volatility has crossed limited and has turned 120 years below, even more than the great depression in 1933. On the other hand, in no events within the history of IHI PLC, the global economy has not been hit so hard that it entirely stopped the manufacturing industries, banned travel, and quarantined people in their homes. This requires the IHI PLC company to strictly take note of the association between the emergence of pandemics and financial crises.

Get 3+ Free Dissertation Topics within 24 hours?

Evaluating precautionary actions involves scrutinizing their effectiveness in mitigating risks and safeguarding against potential threats within the designated context.

Precautionary Actions Evaluation

The first and foremost action of the company took all stakeholders into confidence by promoting a positive wave among the investors and employees. To tackle the collective impact of any pandemic and financial crisis, IHI PLC must devise effective strategies. the company has undertaken all stakeholders to a remarkable consensus that the priority is to sustain the IHI PLC at any cost, and it has provided detailed analysis and information on how this is possible. The company has announced to take all expenses to absolute minimum levels, after which salaries and wages would be the only expenses. Hence, the company has advised a 60% salary for employees and other executives and decided not to fire any of the employees.

Meanwhile, the company has also negotiated with local and international banks to avoid interest and principal payments. Many banks have already agreed on this point. On the other hand, IHI PLC has also undertaken an in-depth and detailed cash flow analysis to prepare for the worst-case scenario. On the other hand, it has also been in discussion with many banks to acquire funds to meet wages and salaries expenses in case the pandemic continues. Therefore, the preventive measures of the IHI have been well received by all stakeholders and can be stated as more appropriate and effective actions.

Before examining adverse effects and potential risks, it is imperative to conduct a thorough evaluation of prevailing market conditions and external factors shaping the business environment.

Adverse Effects and Potential Risks

The adverse effects of the Pandemic on the firm have been listed in the economic implications section, where it has been found that stock markets have turned 120 years low in history and more intense than the great depression. Meanwhile, significant volatility in the stock markets reflects shareholders' sentiments to save their investments, and investors have serious concerns. Similarly, global GDP is expected to decline by 4.46%, which is higher than the economic shock of 2008, in which industries and manufacturing sectors were partially affected due to COVID-19. Meanwhile, transnational trade and foreign direct investment (FDI) have been significantly affected because people are confined in their homes, which has also led to restrictions on international travel. The hotel industry faces more adverse effects since these have been completely emptied, or only a handful of rooms are occupied. Therefore, the hotels' revenues would be almost zero, and they must meet at least wages and salaries liabilities to survive. Meanwhile, a potential risk also exists for the IHI PLC that if this pandemic continues for the next two years, then IHI PLC may not be able to survive further. Therefore, the potential risk for the company is significant.

Cash flows Analysis

IHI PLC has prepared a detailed cash flow analysis for two scenarios; (1) Scenario A and (2) Scenario B. In scenario A, it is expected that the company would make no profit from April to September and then would make a 25% profit from last year’s figures from October to December. The analysis of cash flow shows that the company would have a sufficient amount of cash on hand to meet liabilities until August, but it may face difficulty paying wages. Meanwhile, the company would require additional bank financing to meet salary expenses in this scenario. However, scenario B assumes that IHI PLC would make no revenues from April to December. In this scenario, the company would also go out of cash, or the closing cash balance of the company would become negative in August. Hence, it may also require more additional funds to meet liabilities than scenario A. It is because scenario B generates no revenue, but in scenario A, revenue is expected from September. Therefore, it is determined that in either scenario, the company will be in difficult times and may not be able to pay wages to employees.

The company's past performance shows that it has been facing hard times since its inception, and its share price has also been fluctuating throughout the period. However, the company’s assets have been increasing despite continuously realizing net losses for almost eight years. Therefore, it can also be anticipated to survive in the future. Still, considering the intensity of COVID-19 with other pandemics and financial crises, it is evident that COVID-19 is more serious and contagious than other viruses; hence the consequences would also differ in terms of human losses and economic losses. Furthermore, it is also important to note that when the intensity of COVID-19 is higher, it would also lead to more significant financial losses to the hospitality industry, tourism industry, and aviation. This highlights the direct association between the pandemic and financial crises. There can be two scenarios; (1) if the vaccine for the coronavirus is not prepared for the next eighteen months, then will IHI PLC survive, and (2) if the vaccine is produced earlier, that is less likely than what could be a potential position of the company.

Worst Case – Scenario

In the first case, if the pandemic continues to be as contagious as it has been, the number of cases worldwide tends to rise exponentially as the number of cases has doubled in a single week and crossed 1 million reported cases worldwide. If it continues to be the same, then the quarantine period will be further extended till the virus we contained because, contemporarily, social distancing is only a cure for the virus. In this condition, it is most likely that IHI PLC would have to remain in a zero-revenue scenario until the world is immunized, which will only happen when the vaccine is ready. In addition, 18 months are only projected to develop the vaccine, and it does not account for the mass production period and distribution worldwide. Hence, these 18 months could equal more than 24 months until all travel restrictions are lifted slowly worldwide.

Best Case – Scenario

In the second case, if the vaccine is produced less than the projected time, then this would not be less than at least a year to immunize the world from COVID-19. Therefore, this could be a best-case scenario for the IHI PLC that would take the entire 2020 and the first quarter of 2021. In addition, it is also important to highlight that businesses, including the hospitality industry, would take at least a year to recover and turn to normalcy. However, due to this pandemic, the frequency of travel, tours, and business trips can be affected in many ways. For instance, the corporate business has learned to carry out business transactions, not face-to-face, and during the pandemic use of digital tools has become a meaningful way to carry out business without being face-to-face.

Secondly, distance learning could also emerge and be promoted worldwide to let students be at their homes or anywhere in the world but still be enrolled in any university. In addition, it is also anticipated that the shape of the world could also be changed and the way travel was being used could also be affected. Hence, it is more likely to affect the hospitality industry even after the outbreak is controlled and the virus is contained. Similarly, IHI PLC’s share price has already seen significant fluctuations and has been trading below its share price. Hence, this remains a major concern that the company's share price is sufficient for the shareholders to assume the company would or would have been performing in the future if the efficient market hypothesis is considered.

Conclusion

Businesses are primarily affected in the wake of a global pandemic, followed by those associated with those businesses and communities. The concern remains to be observed until this ends but would IHI PLC rise again is another cause of concern for shareholders. This is because the intensity and severity of COVID-19 are anticipated much more than other pandemics, and economic loss is also greater than the financial crises in 2008. Therefore, from an investor’s point of view, what has to be done to handle their investment? Either opting out would be feasible, or further investment to support survival would be more beneficial to gain value for the investors?

This report was prepared to address these concerns as it highlights that despite the severity and intensity of the virus, it has to end in the foreseeable future anyway. Still, the firm’s survival would be a major issue because it may not be possible for the IHI to continue to pay 60% of salaries to employees. This would also require the company to liquidate some of the assets, acquire a loan and wait for a government bailout package. Therefore, opting out of an investment is not rational since it would only miss the opportunity to benefit from the situation. Thus, further investment would help to survive the company for a period until the virus is contained and the world is immunized. However, uncertainty and risk remain there, which is also a feature of the business without which gain cannot be achieved.

Recommendations and Implications

It is recommended that LAFICO buy some of IHI's shares to support the collapse of the business entirely. The current share price of the IHI is much lower than the nominal value, and it will definitely but may not immediately gain value and reach to actual price in the market. Therefore, it will provide a capital gain throughout the pandemic. After the pandemic, the business can further establish stronger roots to flourish in the global market with an already built diversified portfolio geographically. Secondly, IHI PLC has survived challenging times, such as being on a loss for eight years but still operating. Similarly, it has already taken measures to bring costs to an absolute minimum. Secondly, things may get worse, but if the investment is opted out, there is no alternate option for investment worldwide due to this pandemic. Hence, the LAFICO must buy some of the company's shares to remain firm in hard times and achieve benefits in terms of capital and potential value in the future.

Review the following:

References

Arcgis.com. 2020. ArcGIS Dashboards. [online] Available at: https://www.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6 [Accessed 3 Apr. 2020].

Bender, B., Shafer, J., Harris, J., Kruse, M., Schneider, E. and Shafer, J. 2020. Coronavirus Will Change the World Permanently. Here’s How.. [online] POLITICO. Available at: https://www.politico.com/news/magazine/2020/03/19/coronavirus-effect-economy-life-society-analysis-covid-135579 [Accessed 3 Apr. 2020].

Bertha Coombs, E. 2020. Coronavirus updates: Trump extends national social distancing guidelines through April 30, and a field hospital was set up inside Central Park. [online] CNBC. Available at: https://www.cnbc.com/2020/03/29/coronavirus-live-updates-global-cases-near-700000.html [Accessed 3 Apr. 2020].

Blue swan daily. 2019. 100 countries impose entry restrictions and quarantine measures on South Korea – Blue Swan Daily. [online] Available at: https://blueswandaily.com/100-countries-impose-entry-restrictions-and-quarantine-measures-on-south-korea/ [Accessed 3 Apr. 2020].

Campos, G.S., Bandeira, A.C. and Sardi, S.I., 2015. Zika virus outbreak, bahia, brazil. Emerging infectious diseases, 21(10), p.1885.

Claessens, S., Laeven, M.L., Igan, D. and Dell'Ariccia, M.G., 2010. Lessons and policy implications from the global financial crisis (No. 10-44). International Monetary Fund.

Climent, F. and Meneu, V., 2003. Has the 1997 Asian crisis increased information flows between international markets? International Review of Economics & Finance, 12(1), pp.111-143.

Dan Mangan, J. 2020. Coronavirus could kill more Americans than WWI, Vietnam, or Korean wars, White House projection shows. [online] CNBC. Available at: https://www.cnbc.com/2020/04/01/coronavirus-could-kill-more-americans-than-some-wars.html [Accessed 3 Apr. 2020].

Frieden, T.R., Damon, I., Bell, B.P., Kenyon, T. and Nichol, S., 2014. Ebola 2014—new challenges, new global response, and responsibility. New England Journal of Medicine, 371(13), pp.1177-1180.

Ho, L.C. and Huang, C.H., 2015. The nonlinear relationships between stock indexes and exchange rates. Japan and the World Economy, 33, pp.20-27.

Jackson, C., 2009. History lessons: the Asian Flu pandemic. Br J Gen Pract, 59(565), pp.622-623.

Johnson, S., Boone, P., Breach, A. and Friedman, E., 2000. Corporate governance in the Asian financial crisis. Journal of Financial Economics, 58(1-2), pp.141-186.

Kuznia, R. 2020. The timetable for a coronavirus vaccine is 18 months. Experts say that's risky. [online] CNN. Available at: https://edition.cnn.com/2020/03/31/us/coronavirus-vaccine-timetable-concerns-experts-invs/index.html [Accessed 3 Apr. 2020].

Lienhardt, C., Glaziou, P., Uplekar, M., Lönnroth, K., Getahun, H. and Raviglione, M., 2012. Global tuberculosis control: lessons learned and prospects. Nature Reviews Microbiology, 10(6), pp.407-416.

Lora, J. Brown, D. Palumbo. 2020. Coronavirus: A visual guide to the economic impact. [online] Available at: https://www.bbc.com/news/business-51706225 [Accessed 3 Apr. 2020].

Obstfeld, M., 2012. Financial flows, financial crises, and global imbalances. Journal of International Money and Finance, 31(3), pp.469-480.

Peckham, R., 2013. Economies of contagion: financial crisis and pandemic. Economy and Society, 42(2), pp.226-248.

Presanis, A.M., De Angelis, D., Flu, T.N.Y.C.S., Team, I., Hagy, A., Reed, C., Riley, S., Cooper, B.S., Finelli, L., Biedrzycki, P. and Lipsitch, M., 2009. The severity of pandemic H1N1 influenza in the United States, from April to July 2009: a Bayesian analysis. PLoS medicine, 6(12).

Rustow, D.A., 1977. US-Saudi Relations and the Oil Crises of the 1980s. Foreign Affairs, 55(3), pp.494-516.

Sam Wong, C. 2020. Coronavirus latest: US hospitals come under increasing strain. [online] New Scientist. Available at: https://www.newscientist.com/article/2237475-coronavirus-latest-us-hospitals-come-under-increasing-strain/ [Accessed 3 Apr. 2020].

Skift. 2020. Coronavirus & Travel Industry: Breaking News & Impacts. [online] Available at: https://skift.com/coronavirus-and-travel/ [Accessed 3 Apr. 2020].

Tan, H. 2020. Coronavirus epicentre could 'possibly' shift back to Asia, says, public health expert. [online] CNBC. Available at: https://www.cnbc.com/2020/04/02/coronavirus-epicenter-could-possibly-shift-back-to-asia-health-expert.html [Accessed 3 Apr. 2020].

Travel Daily News International. 2020. The coronavirus affects the tourism industry worldwide. [online] Available at: https://www.traveldailynews.com/post/corona-virus-affecting-the-tourism-industry-worldwide [Accessed 3 Apr. 2020].

World Economic Forum. 2020. This is how coronavirus could affect the travel and tourism industry. [online] Available at: https://www.weforum.org/agenda/2020/03/world-travel-coronavirus-covid19-jobs-pandemic-tourism-aviation/ [Accessed 3 Apr. 2020].

World Health Organization, 2020. Coronavirus disease 2019 (COVID-19): situation report, 67.

Wu, Z. and McGoogan, J.M., 2020. Characteristics of and important lessons from the coronavirus disease 2019 (COVID-19) outbreak in China: summary of a report of 72 314 cases from the Chinese Center for Disease Control and Prevention. Jama.