The Importance of Procurement Strategy & Impact on Construction Projects

January 13, 2021

DBA Value Management Assignment

January 13, 2021

Investigating the availability of homes and the demand among first-time buyers in Hartlepool to understand the local housing market dynamics. This assessment delves into the balance between supply and demand for those entering the housing market.

There are a number of parameters that can have a considerable impact on any housing market, which includes the economic growth, the mortgage rates, the consumer confidence, the geographical factors, unemployment and various other factors.

Abstract

The parameters also play a significant role in influencing the first time buyers, as these parameters can be regarded as the fundamental characteristics of the housing market. The research completed in this paper sheds light on how these parameters affect the housing market, with a research focus on the area of Hartlepool and first-time buyers.

Developing a Competitive Position with a Sustainable Supply Chain

The capacity of the first time buyers concerning purchasing the property in today’s housing market has remained questionable due to the recent economic recessions, and the government has now put-forward various attempts to promote the first time buyers to purchase properties through government-supported programs such as Help To Buy. However, many other concerns/factors are related to the first time buyers, and efforts have been made in this research to link and highlight these factors through a ‘client’s perspective’. Therefore, after completing a detailed literature review on general parameters of housing markets and of / specific to Hartlepool, primary research was undertaken in which experts of the industry along with the actual first-time buyers were interviewed and data was collected through questionnaire forms distributed amongst the potential first buyers.

The results of this research indicated that various concerns must be addressed to ensure optimum participation of the first time buyers in the housing market. A detailed review of Hartlepool market was completed, and it was found that although the area is self-sustained, it still needs further developments for it to grow in the prospective future. The survey results also indicated the prospective first-time buyers on factors such as mortgage rates and calculators, ease of lending, reliability on financial assistance, dwelling requirements/needs and various other factors that can potentially influence the decision of purchasing a property in the area of Hartlepool.

The complexities of the housing market in the United Kingdom have been a matter of concern for the last many years, as it has been subjected to various uncertainties in the last few decades.

Chapter – 1; Introduction

The highs and lows in terms of economic bubbles, rising market prices, uncertainties over the interest rates and the ratio of demand and supply in the subject market have been the fundamental source of these complexities (Muller et al., 2009).

Impact of Outsourcing on Customer Experience in Supermarkets/Hypermarkets

Although the stakeholders of this market have been primarily the investors who purchase properties for business purposes, the influence of first-time buyers in the market cannot be ignored. The first-time buyers are the proportion which can stabilize this industry as they are considered to be potential end-users of residential properties. Another factor related to these users is that they can reduce the impact of investors in the housing market, which in the end reduces the chances of an ‘unmanaged rise of house prices’. However, the increasing uncertainties and complexities of this market have undermined this potential and have consequently resulted in a lack of confidence or clarity in the minds of first-time buyers(Quigley and Raphael, 2004), however, the situation has now started to improve due to better policy implementation and through a tailored government support programs.

There are mainly three different goals that are aimed by the public policy devised for the housing market. One – roof and accommodation should be provided to all the families. Two – to boost people to take ownership of their houses. Three – to encourage the construction of houses. In the past, the main reason for social housing had been to provide accommodation at a reasonable price for all the people while maintaining a specific standard. The government has been providing grants for the development of social housing. In Tayman's terms, housing prices are an indicator of demand and supply methodology if all the other factors are kept constant. An increase in the supply of houses would see the house prices fall while an increase in the demand for houses would see the prices of houses go up (Gan and Hill, 2009).

In the UK, the population is increasing, and this is the real income of the people. The trend has been towards a smaller size house which has resulted in more houses than needed by the current population. TFinancialfreedom has resulted in more money being taken from the banks for purchasing touses (Himmelberg et al., 2005). In the long run, owning other forms of assets has dampened as compared to houses because of their falling annuity and low interest rates for house purchases. In recent times, the availability of credit and the option of borrowing money has had a significant impact on the demand for houses. Since the supply of houses has been almost constant in the past few years, the increase in demand for the house usually seeps into the rising prices of the houses. In the long run, the reaction of the supply of houses to the increasing prices will mainly depend upon the availability of land, which is dependent on the laws of the country, and the eligibility and competitiveness of the constructors (Tsai, 2013).

According to TTransactiondata from HMRC, the housing market started to fall in 2007. Along with that, a dramatic fall was also observed among the other barometers of the housing market. However, these barometers have stabilized again since 2013. There was a sharp decline in the monthly housing transactions from 150,000 in 2006 to 52,000 in 2009; which eventually started increasing in 2010-11 to 73,000 before stabilizing to 100,000 in the last quarter of 2013 (HMRC Transactions data, 2014).

The increasing house prices have recently been a matter of concern because of two fundamental reasons. The first is that there might be speculations that the increase in prices might not be due to the economic development of the area, rather it might be a bubble which might bust and will cause financial instability in the area and might affect household consumption. Secondly, even if the rising prices are because of economic development, the rising prices might make it extremely difficult for the majority of the people to own a house. This way a lot of potential clients, especially first-time buyers would be left without their basic right of shelter and accommodation. Apart from that, increased house prices have a direct impact on construction companies and household behaviour. It is known that house prices and household consumption are strongly interrelated but it is yet to see the precise effect of house prices on the consumption of houses. The changing house prices may also affect household savings because of mortgage rates. Also, the labour market is affected by the varying prices of houses since household wealth is affected by changing prices (Tsai, 2013).

The demand for houses is affected by a lot of factors. Some of these include;

- The size of the population,

- The population distribution,

- The relative price of the house as compared to other utilities,

- TConsumerconfidence, geographical factors,

- The real income of the people, and the availability of the mortgage to the people, and

- The availability of suitable/demanding dwellings in the market

The expected prices as well as the dwelling types are also important in the demand for houses as they attract or repel the potential clients towards the housing market. If the prices are rising then the expected benefit of entering the market is increased i.e. asset value is increasing. Furthermore, if the supply of demanding dwellings is available in the market, that can enhance the rates of the transaction in the housing market. Apart from that, the down-payment costs also increase because of the increased expected prices. The recent trends in the housing market greatly influence the expected prices of the houses which in turn affects the price volatility. It can be predicted that in the long run, house prices would be mainly affected by the real incomes of the people and the geographical changes in the region.

But how does this dynamic nature of the housing market affect first-time buyers?

This is the primary research question aimed to be addressed in this research. The focus of the research is to analyze all the factors that can potentially influence first-time buyers and review the governmental policies that provide support in this regard. Since this is an extensively dynamic topic, the area of Hartlepool has been selected to investigate the demographic factors and review the current market conditions. This strategy has been adopted to limit the scope of research and develop an understanding of how certain factors can influence the performance of a local market. The following are the primary aims, objectives and motivations of this paper.

1.1 Research Aims

The primary aims of this research are;

- Develop an understanding of the Housing Market in the K, with a special focus on the locality of Hartlepool

- Identify the fundamental parameters/drivers of the housing market that influence this industry

- Investigate the major concerns, including the complexities of the housing market, such as the impact of interest rates, supply and demand balance etc.

- Through research, analyse these parameters about the first-time buyers. This is to be achieved through primary as well as secondary qualitative research.

- Determine what influences first-time buyers on property purchases

1.2 Research Objectives

The objectives of this research are;

- Investigate the fundamental attributes of the housing market in the area of Hof Hartlepool

- Explore the implications such as affordability, recent market trends and other influential parameters, relating to first-time buyers

- Assess the quality of the Help to Buy scheme and how this affects first-time homeownership in today’s market

- Examine the pros and cons of new builds and refurbishment properties

- Assess the immediate and future development plan of Hartlepool

- Analysis of the Hartlepool average wage and average house price, comparing with the average wage in the UK and average house price in the UK. Discuss and suggest how these factors may influence the first buyers

- Undertake primary research to obtain views of first buyers and discuss their behaviour, expectations and potential about the housing market in Hartlepool

- Analyse the funding of this research and highlight the key findings from the responses from first-time buyers

1.3 Motivation for Research

The motivation for this research came from the apparent imbalance between the supply and demand of the housing stocks in Hartlepool. It has been promulgated in the media that the demand for houses, especially new builds has been on the rise with the cost ranging from £115,000 to £150,000 for small to medium-sized dwellings, with developments in progress at various sites and many plans dismissed by council due to flooding concerns. However, the refurbishment properties with prices ranging from £70,000 to £80,000 have been reported to be difficult to sell. Furthermore, the impact of governmental efforts/schemes such as help to buy and the lower current mortgage rates may have influenced the current dynamics of the Hartlepool housing market. These findings have motivated the researchers to further investigate the housing market of Hartlepool along with various factors that may have influenced and changed its course of direction; including the role of first-time buyers.

This research aims to provide investigative analyses of Hartlepool’s housing market, its requirements from the perspective of first-time buyers, the impacts of various factors, and the need for future developments. This research can also be used as a guide to undertaking further studies on the factors that have influenced the housing market of Hartlepool at large and the potential first-time buyers.

Before continuing to a technical/specific literature review on the housing market of Hartlepool, it is imperative to review the general literature that has been published in the last many years on the factors/parameters of the housing markets across the globe.

Chapter – 2; Literature Review

This section of the paper thus presents the literature review in the form of background analyses on the fundamental aspects of any housing market. This was completed to develop an understanding of key elements of the larger dynamics of housing markets across the globe.

2.1 Background Analyses of Housing Markets

Since the beginning of the industrial era, civil society has always been affected by the prices of the houses and the ups and downs of the overall housing market. So, it becomes extremely important to understand the fundamentals of the housing market along with the pricing of individual houses and housing societies, and how the parameters associated with it affects the residents of the society. According to the literature reviewed, the housing prices in the UK reached its lowest mark in the 1990s after which it started to increased again and reached their apex in 2007. Since 2007, the market has shown a downward trend, however, the last few years how now shown significant improvements (Institute for Fiscal Studies, 2014).

In recent times, questions have been raised in housing societies of some countries because of the rapid rise in prices leading to overvalued prices. This, in turn, affects the people who want to buy a new property. Because of the rising prices, buying-for-selling phenomenon has become extremely common. People pay higher mortgage values for a house and expect to sell it to another client for even higher mortgage value. The prices have generally increased as a result of demand and supply factors along with mortgage lending. Interestingly, the same aspects have also been the reason behind the downturn of the housing market. It can be seen from the crash of housing society in the UK in 2007 where the main culprits were the financial lenders and stakeholders managing the market. Moreover, these factors may have also contributed to halting the poetical of first-time buyers as the housing prices were not economically viable/affordable for the normal working class of the UK (Tsai, 2013).

In the research conducted by the UK Housing Market Economic Review, Gavin Cameron pointed out that the sudden rise in the prices of houses was mainly because of the fragile nature of the UK housing market. He reasoned by stating that most of the houses in the UK can be re-mortgaged at variable interest rates due to which the loan-to-value rates are very high in the UK and selling the house after purchasing it from a different seller is pretty easy. Furthermore, the variations in the house price signify the fragility of the UK market. This makes variations in the interest-rate important because of the variable interest loans prevalent in UK housing markets.

Housing is a unique type of property because it has applications in the investment category as well as the consumption category. A person can get exposed to the fluctuations in the housing market if they own a property. However, if the property is bought for the sole purpose of investment then the asset pricing model can be applied to it. But it is still very difficult to determine the basic price of that house since every household has unique characteristics like the location, interior setup, construction design etc. So, it is extremely difficult to place an intrinsic value on a house or any property (Reed and Wu, 2010).

A lot of studies were carried out to find out the relationship between the economic conditions and the prices of the houses. In 1976, Gottlieb theorized that long swings in economic activity are directly related to the long swings in construction prices and development. In recent studies, efforts have been made to find out how the change in prices over a period of time is related to the economic shocks incurred by the market. These studies range from explaining the effects of changing prices on the market prices to explaining the economic effects on pricing in specific regions.

Different authors have used different approaches in order to find out the basic model of the housing market. One study, carried out by Hui and Yue in 2006, used external variables from macroeconomics to outline the fundamental of the housing market. In another study carried out by Case and Shiller; the researchers, in order to check the value and return of houses, used time-series coefficients along with some other independent variables. The relation was found to be positive in case of excess tax returns during 1970 and 1986. In 2003, Hofmann found that economic growth, interest rates, and equity prices have a direct impact on the prices of the houses. On the other hand, a regional study was conducted by Egert and Mihaljet in 2007 in 27 OECD and European countries. The results revealed that infrastructure/housing economics is directly related to macroeconomic factors, governmental policies and financing of housing societies.

As the literature review revealed, there are several studies with a varying degree of understanding of factors associated with the housing market. House pricing was a much talked about issue in recent years, especially after a serious financial crisis In the United Kingdom and the United States. Tsounta suggested that the regulatory bodies should keep a check on the housing market and it must be made sure that the dwellings are neither undervalued nor overvalued so that the market economics remain stable and any imbalance can be avoided. Since house pricing is an economic business, any changes will have a direct impact on the outlook of economic growth and the financial sector. The consumption growth increases because of the increase in housing prices. This is because the housing properties have a more considerable effect when compared to other financial assets.

This positive change on the consumption rate of households due to increased housing prices is also confirmed by Girouard and Blondal (2001) who carried out their studies in OECD countries. In a paper by Trichet in 2003, it was stated that variations in house prices can impact macroeconomics by changing the consumption and investment in the household markets through wealth and balance-sheet effects. Peng, Yiu and Tam (2005) concluded that higher house prices are an indication of faster growth in the economy. The house pricing is an important financial variable which controls the market and effects the consumption rate.

The bubble formation in the housing market has also been much discussed when it comes to housing markets. However, it is important to note that increased housing prices are not always an indicator of larger housing bubbles. There exists a differentiation between the overvaluation of houses and the house pricing bubbles. The overvaluation of house pricing points to the fact that current house prices are valued above their basic values. Whereas, the development of the house pricing bubble refers to the fact that house prices are increasing on the belief based upon the future movement of house pricing. This explains that house pricing bubbles cannot be explained by statistical data. House prices can, in some cases, be overvalued because of the friction found in the market. Explaining the concept of house pricing bubble, Brunnermeier and Julliard in 2008, stated that an increase in house pricing can be labelled as a bubble when the increase cannot be explained using short-term dynamics and is mainly based upon on an overly optimistic expectation about the future prices in the household market.

2.2 Fundamental Housing Market Factors

To further investigate the impact of distinct factors on housing markets of different countries, much of the literature was reviewed with special focus on fundamental variables such as interest rates, mortgage rates, supply chain, affordability, price to income ratios etc., which have been outlined in the sections below;

a. Housing Market and household Income

In 1990, Case and Shiller (1990) presented their study in which they found a positive correlation between housing prices and tax returns with per capita income. The study included the data taken from Dallas, Chicago, San Francisco and Atlanta from 1970 to 1986. Peng, Yiu and Tam concentrated their study on China’s house market and found that there is a two-way relationship between house prices and the GDP of China. Leung, Chow and Han (2008) suggested that because of the smooth rise in the household income, the steady value of the housing has increased in the Hong Kong market. Milne (1991) also found a direct relationship between house prices and income. Similarly, Hui and Gu also found that house pricing was a direct consequence of the buying power of the people. Case and Shiller (2003) concluded that the per-capita income of the people can fully explain the increase in the prices of houses.

b. Housing Market and Vacancy Rate

It was observed by Hui and Yue that an oversupply of a certain commodity leads to a decrease in the selling price of that commodity. In house market, the oversupply is observed in the form of large vacant stocks. An increase in house prices may lead to an increase in the vacant stocks because of the lower affordability ratio of the people. Peng and Hudson-Wilson (2002) found an inverse relationship between office prices and slot rates. The study took into consideration a number of variables which included price indicators, office vacancy rate, the operating income and the basic economic index. They concluded that higher prices are indicative of demanding markets because higher office prices would mean fewer vacancy rates which lead on to form tight markets.

c. Housing Market and Mortgage Rate

The money borrowed by people for buying houses has a specific interest rate attached to it. That interest rate is called the mortgage rate. In 1982, Follain indicated that high mortgage rates would eventually lead to lower housing prices because the problem of houses’ liquidity increases with increasing mortgage rates resulting in less demand of houses, thus lower house prices. Thus, the demand for houses can be steered by the availability of the capital. A result which indicated an inverse relationship between the mortgage rates and house prices during 1989 and 1997 was reached by Wong, Hui and Seabrooke in their studies in 2003.

However, when the markets collapsed in the 1990s, the lower interest rates corresponded to lower house pricing. This positive mortgage relationship with the house pricing was covered up by the predictable losses in capital, therefore the decreased interest rates may not be able to prompt the house pricing. Case and Shiller suggested that the mortgage rates may not be of significant importance in the housing market, as a decrease in house prices may also be possible because of the presence of a weak economy and the Federal Reserve may lower the rates in order to counter that effect.

d. Housing Market and Housing Supply

It is generally perceived that an increase in housing stock leads to the lowering of house prices. A study was carried out in Haifa by Van der Vlist, Czamanski and Folmer in 2010. They found, using the Auto Regressive Distributive Lag (ARDL) model, that during January 1989 and June 1999 the housing stock and house prices had a significant negative correlation between them. In 2007, it was suggested by Glindro et al. that increased land supply results in decreasing the prices of houses, which was in agreement with another study carried out by Peng and Wheaton in 1994 in which they, after using an econometric method, found a negative correlation between land supply and house prices. It is sometimes contended with the fact that a reduction in land price may lead to expectations of higher earnings because of higher housing rents. The house prices in the private market are also dampened by the land supplied by the government to people for private use. (Lum, 2002)

e. Housing Market and User Interference / Behavior / Response

The housing market consists of a variety of qualities and prices. When the homeowners have made a remarkable profit in their existing homes, then they make an improvement in their quality of living. (Ho & Wong, 2006). Homeowners are able to shift their trading from smaller to bigger and better quality houses once they have accumulated a sufficient amount of wealth. (Stein, 1995; Ortalo-Magne and Rady, 2004). The change in housing prices causes a rise in down payment that increase demand and cause the prices to go up eventually. (Stein, 1995) as a result of this, a vertical chain reaction will start across various house sections on the property ladder (Otalo-Magne&Rady, 2004). If the prices of existing homes go up, the flat owners will want to switch to better new homes by trading their old homes after the down payment and mortgages of new houses are covered.

f. Housing Bubbles

The housing bubbles exist in the housing markets and there is a variation in their length. There are 2 ways which can end the bubble - an abrupt collapse or transformation to another regime. Muller et al (2009) suggest the reasons which play a role in creating the housing bubble. This includes a change in demand and supply, change in the common population pattern, progress at both individual and collective level and changes in buying power of consumers. Case and Shiller (2003) argue that the main components for the creation of bubbles with respect to the demand side are statistics, changes in job and growth in yearly earnings and alteration in financial techniques, characteristics of area and interest rate, whereas the supply side consists of the expenditure incurred on buildings and equipment’s and “Industrial Organization in Housing Market”.

According to Allen and Gale (2000), there are 3 different phases of housing bubbles. In the first phase, consumers are subjected to more money and financial relaxation and fewer credit constraints by the rise in price in real assets. The first phase then leads to the second phase when it has completely matured. Phase one usually lasts for a few years until the bubble has inflated. In the second phase, the bubble bursts and the price of real assets fall in the short run-weeks or few days. The last phase constitutes of loans and banking crisis which creates a problem in the economy for a few years. This argument is also supported by Zhou and Sornette (2003), Gouldey and Theis (2012) and Muller et al (2009).

According to Herring and Watcher (2002), the time lag in construction is the reason behind the inelastic supply of asset such as houses. In the short run, when the supply is inelastic, the increase in demand for houses causes the price to rise at a very high rate. After the price has risen to a very large extent, the cost of equipment and time span in the market goes up, vacancies increases and prices rise up gradually, and as result downward, stickiness takes place (Case and Shiller 2003). This was also supported by Glaeser et al. (2008) who suggested that a continuous rise in housing prices indicate an increase in housing supply which shows that the supply will exceed demand at some point in time. The effect of the demand is decreased as a result of which the prices fall and hence the bubble bursts.

According to Gouldey and Theis, some external uncontrollable forces such as government initiatives to expand the home ownerships also influence the housing demand. The number of houses demanded will amaze the developers and builders. This will cause the builders to construct new houses by anticipating the demand of consumers. The bubble can be prevented if the housebuilders can estimate the demand for the number of houses without committing any error. Since no such accuracy is met, a housing bubble is created.

g. House Affordability

The definition of House Affordability is really simple. It means the ability to purchase a house (Linneman and Megbolugbe, 1992). Quigley and Raphael described the vague property of affordability. Their research suggested that affordability covers a lot of issues of distribution of housing prices and quality, income, the borrowing capacity of households and the choice for the consumption of other goods. These issues are important to analyze the definition of affordability. MacLennan and Williams (1990) have also presented their own view of affordability. Affordability is concerned with achieving some basic standard by paying some price or rent for it which does not create any burden for the householders. In other words, it means that when householders buy a place for a price and this price does not have any effect on their lifestyle (Stone 1993). Freeman et al (1997) define affordability by explaining the relationship between the cost of house and income of the householder.

h. Housing Prices to Income Ratio

It is the measure of the affordability of a house in a specific region. It is the ratio of the mean of both housing prices and the annual income after tax of a family. It can be written in the form of a percentage (Messah and Kigige 2011). This ratio helps in measuring the average purchasing power of families (Himmelberg et al 2005). This has also been stated by Ndbueze (2009). Flood (2001) stated that the ratios of 3 or 5 are normal and are considered as the best measure of force in the housing market whereas, Reed and Wu (2010) suggested that the most accepted ratio that measures the affordability criteria is 3. There are different rules for interpreting the affordability ratio. This is the reason the analysis of these ratios have become difficult, also, the ration excludes the changes in taxes, quality of houses and interest or mortgage payments of houses (Hancock 1993; Freeman et al. 1997; Lerma and Reeder 1987; Ndubueze 2009).

i. Debt to Income Ratio (Mortgage Cost)

It is the ratio of payment for a mortgage and the after taxed income of a family in the concept of housing. This ratio is important because it helps in measuring the total homeownership expenditure. The mortgage payment in the numerator in most cases is a percentage which represents the monthly household income. If the ratio is too high than what is considered normal, then it means that the households are contingent upon the increased property value to repay their debt (Messah and Kigige 2011; Gan and Hill 2009). In simple words, it can be concluded that this ratio helps in measuring the capacity of households to get rid of their mortgage payments. (Tsai 2013; Gan and Hill 2009).

Following texts are related to methodology of study.

Chapter – 3; Methodology

Three different but interrelated methodologies have been adopted in this research, which are;

- The first approach was conducted to develop an understanding of the general housing market and the associated parameters. This was accomplished in the Literature review chapter of this paper, in which research conducted by various researchers from around the globe was reviewed and critically analyzed. The findings literature/information, which was relevant to the topic of this research were outlined and discussed.

- The second approach is aimed to investigate the factors that influence the housing market in Hartlepool, which is completed under the Results & Analyses chapter of this paper. This includes desk-based research on the housing market of Hartlepool, outlining the influential factors such as housing prices, affordability, interest rates, government schemes and supply and demand parameters. The focus of this research is aimed at the first time buyers, however, it is important to note that the distinction between investment category as well as consumption category is difficult when it comes to analyzing the published data by Borough Council and Strategic Housing Assessments

- The third approach has been aimed to collect data of the first time buyers through conducting interviews and requesting them to complete in-depth questionnaire sets. This was completed to gain access to views of the first time buyers of properties in the area of Hartlepool and the market experts so that the internal perspective of this proportion of end users can be obtained. Since not much research has been conducted to obtain views of the first time buyers, it was important for this research to develop a detailed but easy to complete questionnaire, which comprises of fundamental questions in relation to the housing market in Hartlepool. This was undertaken to establish a reasonable connection between the factors analyzed in the literature review and actual respond of the end-users

The results obtained from the literature reviewed, interviews conducted and the completed questionnaire were assessed to understand the actual market variables in the Hartlepool area, in terms of supply and demand relationship. Furthermore, the response of the first buyers was evaluated to address the research questions;

“What factor influence the stakes of the first buyers in the Hartlepool housing market?”

The qualitative primary as well as secondary research methods provided support in establishing an extent to which the current market is facilitating the first buyers, and highlighted the key areas of concern from the perspective of “internal views” of first buyers”.

In the context of this study, it is important to outline the confinements as well as the strategies that have been adopted to complete this research. First of all, the focus of this research was the area of Hartlepool; and the questionnaires were handed over to the potential first buyers who were looking to purchase the property. This may imply that there could be numerous potential customers who were thinking to purchase the property but have not consulted the agents at the time of data collection, hence have not participated in this research. This is primarily because due limited time and scope of this research, the first buyers were approached through property agent of the locality, as the door to door approach was not possible within the limited scope of this study. Furthermore, views of property experts in the area of Hartlepool were also recorded in this study.

Find Out Quality Intellectual Property Law Dissertation Topics

Moreover, the qualitative methodology of this research may implicate that any declaration, evaluation and reflection of research results may not be considered as official results, as these are qualitative analyses and opinions of individuals. Moreover, as suggested earlier, a difference of opinions in terms of the expectations and requirements may change for the majority of the population that have not participated in this research.

Chapter – 4; Results & Analyses

The literature review section of this paper presented the details of how various parameters which influence the housing markets around the globe.

4.1 Desk Based Research; Analyzing the Hartlepool Market

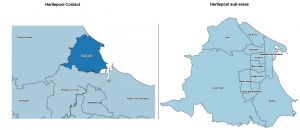

This section of the paper reviews these parameters in the area of Hartlepool, which is the primary research focus of this paper. This following is the map of the Hartlepool;

Figure 1; Map of Hartlepool (source: SHMA, 2015)

Demographic Factors; Comparing Fundamental Parameters

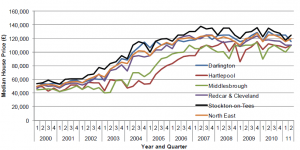

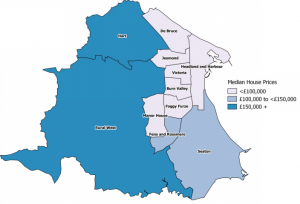

Analyzing the data obtained from the Hartlepool Borough Council, It was observed that the housing prices in this area have remained on the lower side as compared to the median housing prices of its adjacent areas, as shown in the figure below;

Figure 2; Median housing prices in Tess valley (source: Borough council, 2014)

According to the more recent results published by SHMA in 2015, the Hartlepool median house prices in terms of the ‘sub-areas’ was presented as follows;

Figure 3; Median housing prices Hartlepool Sub area (source: SHMA, Hartlepool, 2015)

Analyzing the housing market trends, it can be observed that house prices in the areas of Rural West and Hart are more expensive. Furthermore, it was also observed that Hartlepool has been subjected to long term effects of the economic downturn when the market suffered a collapse between the years 2007 and 2008. During the year 2011/12, the median housing prices were in the range of £110,000 in Hartlepool, whereas prices in London were £180,000 and in North East, the median was in the range of £120,000 (SHMA, 2015).

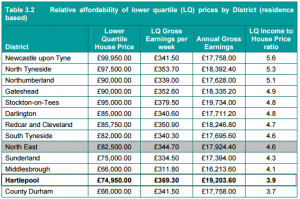

It is also important to investigate the housing market trends in terms of the relative affordability characteristics. The quartile house price, annual earning and income to house prices ratios by the district was collected by Annual Survey of Hours and Earnings 2013; land registry price 2013 and presented in the report by SHMA as;

Figure 4; Affordability characteristics (source: Annual Survey of Hours and Earnings; land registry prices, 2013, edited using MS paint)

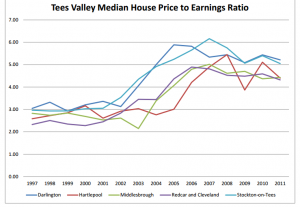

As demonstrated from the table above, it can be seen that Hartlepool is one of the most affordable districts as compared to other regions, with the house price being 3.9 times the lower quartile gross earnings of residents. Similar, the median house price to income ratios of Hartlepool was presented by Tees Valley Housing Market Indicators;

Figure 5; Median house price to income ratios, Hartlepool (source: Tees Valley Housing Market Indicators, 2015)

The house price to income ratio trends of the Hartlepool suggests that the annual incomes of the residents have slowly increased and/or the affordability ratios have fallen. The median income to house price ratio of 4.69 in the year 2011 suggests that the Hartlepool Borough is relatively more affordable as compared to other districts of the UK.

The data published by Census in the year 2011 suggested that Hartlepool area can be considered as self-contained or stable, as 80.20% of the household movements before 2011 in the Hartlepool were originated from within the Hartlepool Borough; which means that the area has not been subjected to additional load/demand of dwelling supplies. This could implicate that the area has not been able to attract residents of other districts through economical or other opportunities.

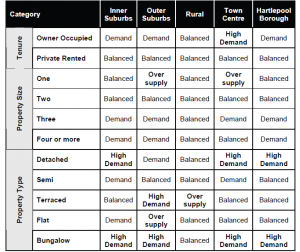

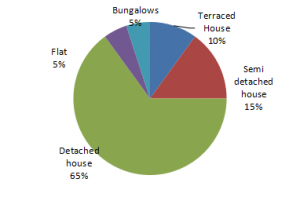

In order to further analyze the demand and supply of available dwellings in the district, it important to present the available data in terms of availability of dwelling types, and their demands under each sub area. The report published by Tees Valley SHMA illustrated the demand and supply balance of dwellings in this area as follows;

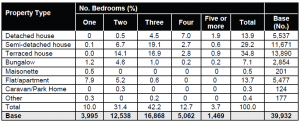

Figure 6; Hartlepool housing market supply and demand (TVSHMA, 2012)

As it can be reviewed from the data above, the current dwelling stocks can potentially influence the demand and needs of future housing. The Tees Valley has been noticed to have a balance between the supply and demand of houses in many categories. However, the table above shows that there has been an observable shortfall of detached houses, terraced buildings and bungalows in the inner suburbs and outer suburbs respectively.

Furthermore, according to the 2012 TVSHMA observations, the dwelling stocks in the area of Hartlepool are as follows;

Figure 7; Hartlepool dwelling stocks (source: TVSHMA, 2012)

Reviewing this data, it can be observed that a major proportion of dwelling constitutes of semi-detached houses and terraced houses (about 64%), whereas there are only 13.86% stocks of detached houses in this area. This finding further strengthens the arguments that there is a probable imbalance between the availability of stocks and the market demand in the Hartlepool’s housing market, which is further investigated in the later sections of this paper

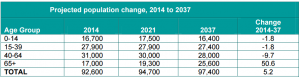

As indicated in the literature review chapter of this paper, the population growth can also play a significant role in determining the trend of the housing markets. According to Office of National Statistics, 2012, population projections show an increase of overall population in the area of Hartlepool, however, the population for the age 15-39 years is expected to remain the same.

Figure 8; Projected Population of Hartlepool (source: ONS 2012-based population projections)

The important demographic factors that will govern the house prices in the future were also illustrated by TVSHMA. The population rising at a rate of more than 5.8% in the Tees Valley. The ratio of older people is also expected to rise. Thus, the area will observe an increased demand in a number of houses according to DCLG forecasts. According to the TVSHMA Final Report of 2012, it was reported that there were 28% couples with children, 19.1% single adults, 16.4% couples with no children, 11.2% lone parents, 10.9% singles over 60, 10.4% couples over 60 and 3.8% another type of people living in the households. These demographic factors are accounted for all type of households and special attention is needed for the families and older people households, which demonstrates that a good proportion (especially single adults and couples) may as well consider moving houses in the prospective future.

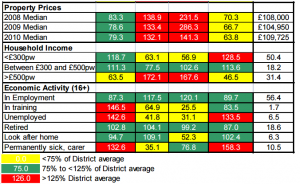

Economic Factors; Mortgage Rates, Earnings & Help to Buy Schemes

The recent publications of TVSHMA, 2012 show that 58.4% of the household reference residents are economically active and are underemployment, whereas 19.8% are retired and approximately more than 5.4 % are unemployed. However, according to the Tees Valley 2012 Strategic Housing Assessment Final Report, the employment rate was 6.5%, indicating the value is at least 125% of the district mean, as shown in the figure below;

Figure 9; Hartlepool sub-areas attributes (Tees Valley 2012 Strategic Housing Assessment Final Report)

Figure 9; Hartlepool sub-areas attributes (Tees Valley 2012 Strategic Housing Assessment Final Report)

Furthermore, it was suggested in the annual survey conducted by ONS in 2013 that the lower quartile earnings in the area of Hartlepool in comparison with other regions has been as follows;

- Hartlepool: £19,205

- North East: £17,924

- England: £19,323

Whereas the median incomes for the year 2013 have been;

- Hartlepool: £24,721

- Regional median: £24,560

- National median: £27,076

These values suggest that the lower quartile earnings of Hartlepool are comparatively in balance with England’s overall average, and the area lacked behind in the median incomes as compared to the national average. However, it is important to note these values along with the high values of unemployment rates may not necessarily impact the affordability characteristics as the houses prices in this area are also low, resulting in lower house prices to income rations, as previously presented in figure 4.

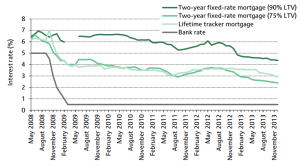

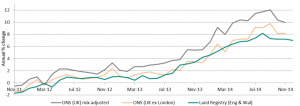

As concluded previously during the literature review, the mortgage rates play a pivotal role in any housing market, therefore it is important to demonstrate the current trends of the lending rates of the UK’s housing markets. According to the Bank of England, there has been a significant decrease in the UK lending rates, as indicated from the figure below

Figure 10; UK lending rates (source: Bank of England, 2014)

The figure above shows that lending rates have decreased to below 5% since 2013. Furthermore, according to the Homes and Communities Agency, Strategic and Market Intelligence report of January 2015, the overall economy UK is strengthening as GDP and employment is increasing. This has eventually resulted in an increase in housing prices across the UK, as suggested in the figure below;

Figure 11; Trend of Housing prices in the UK (source: HCA, 2015)

Another important finding in this review was that there has been a positive change of 5.6% in the total mortgage lending amounts in November 2014 to the first time buyers, as compared to the amounts of November 2013 (HCA, 2015). This could be because to back homeownership, the Government introduced a new policy named ‘Help to Buy’ in their March 2013 budget. It has two main clauses. The first one is that government free loans of up to 20% were offered to the buyers of new homes in the form of Help to Buy: equity loans. This clause was introduced in April 2013. The second one was the introduction of Help to Buy: mortgage guarantee which gave the mortgage lenders the liberty of buying insurance for high loan-to-value (LTV) mortgages (Institute for Fiscal Studies, 2014)

Although the lenders have been providing insurances since October 2013, the government started this insurance policy in January 2014. These schemes would allow the buyer to buy a home at just 5% initial deposit. Since there is no lower limit of house income for buying the houses, these schemes are available for both the current homeowners and the new ones. These properties are sold for self-residential purposes only and cannot be rented out. A house worth £600,000 can be bought using these policies. However, the Help to Buy: equity loan can only be used in case of new houses. It does, however, it requires zero-interest for the first five years. What happens is that the government buys 20% of the house owns property and charges zero rent for five years. A fee of 1.75% on the loan amount is charged by the government in the sixth year. From next year onwards, if there is still some amount to be paid, the government charge fee increases by the Retail Price Index (RPI) plus 1%. While repaying the loan, the owner must repay his loan before selling his house or at the end of the mortgage, depending on one that comes first. Another option available is that at the end of the first year, a minimum of 10% of the total amount of the property can be repaid. The outstanding equity loan must be repaid at the time of selling the house (Help to Buy, (2013); UK Government).

The mortgage schemes aim at increasing the supply of high LTV mortgages by giving government insurance to the buyers against any losses. This allows the lenders to minimize the losses incurred in case of repossession of losses. Just like the case with the Help to Buy: Equity Loan, this scheme aims at increasing the number of people who can afford a house by minimizing the initial deposit. However, it is not intended for increasing the number of new buildings

Let us see a hypothetical example of a household which uses this scheme. The assumed household income is £50, 000 while the monthly loan is around £39, 000. If the house is to be bought using the traditional method of buying with a 75% mortgage, then an extra deposit would be required. This would mean that they have to wait another five years for the transfer of ownership, provided they save an additional 20% of their income per annum. Now, if the scheme method is to be followed, then the property can be purchased using a 5% deposit and a 95% mortgage. The household will have to pay £1,080 as compared to £780 in the traditional case. This scheme is usually used by those households which have above-average incomes as compared to the general population but lower income than those who usually purchase houses on its face value.

4.2 Primary Research; Questionnaires & Interviews

The previous section presented details of the Hartlepool’s Housing Market Indicators such as housing prices, interest rates, affordability etc.; in comparison with other areas of the UK. The following section outlines the finding of a series of interviews as well as questionnaire, primarily from the potential first-time buyers of residential properties in the Hartlepool. This was completed to obtain the perspective of the buyers with regards to the housing market of Hartlepool

A direct interaction/approach with the first time buyers was not possible as it would have required extensive time and effort along with other resources. Therefore, well-known estate agents and constructors/builders in the Hartlepool area were approached for his purpose. Those who were willing to help in this research were provided with the details and extent of this study. Out of the 14 associations/companies/agents approached, 6 of the agents agreed on the terms that their business confidentiality will have to be maintained. The supporting association were requested to arrange interviews with the first time buyers of properties in Hartlepool (willing clients) and hand over the questionnaire for them to complete.

Real Estate Dissertation Topics

The sampling of participants was accomplished by asking the following question before handing over the questionnaire to complete. This was done to avoid/reduce irrelevant sampling and increase the validity of this research.

“Are you a first-time buyer who wants to obtain a property within the next 12 months?”

The clients who responded yes to this question and also showed a willingness to complete the questionnaire was provided with a copy of the questionnaire on the site. The questionnaires were originally sampled for four weeks in February, but due to low respondents and low demand in the interest of properties for first-time buyers, Ii was decided to ask the agents and developers if it would be possible to sample the period of March, as it was indicated by the agents that the month of March is relatively busier as compared to February. All the 6 agents agreed to support this research for a four week period in March 2015.

The questionnaire included a total 26 simple multiple-choice questions which were easy to complete in a short time interval; to ensure that participants are able to provide information with ease while spending just a few additional minutes at the agents’ facility. A total of 20 completed questionnaire forms were obtained from 6 different agents, although more than 35 potential first-time buyers were requested to complete the questionnaire. The details of the questionnaires are documented in Appendix 1.

The interviews were conducted in the month of February 2015. The interviews were structured to indicate the views of first-time buyers on the housing market of the Hartlepool and the factors associated with the ‘ability to purchase housing in the current economy and governance structure’. Interviews were also conducted with the representatives of the leading estate agents/construction builders, to obtain views of the professionals in the housing market of Hartlepool. Transcripts for interviews were also recorded for some interviews, to showcase how the actual interviews were performed. One example of the transcript has been presented in Appendix 2.

4.2.1 Interviews

A total of four interviews were arranged/conducted with the first time buyers. One of the interviews was arranged on the premises of the agent, one at a construction site and two interview sessions were arranged over the phone. The table below outlines the scope of discussions, however, these were not specifically asked all the participants as a general discussion were completed within a limited time. Each interview was conducted for about15 to 20 minutes. Refer to Appendix 2 to review an example of how the interviews were conducted.

Table 1; Interview Session scope of discussions

Interview Questions / Scope of Discussions |

1. Do you work in Hartlepool? |

2. Do you feel employment in Hartlepool has increased or decreased in the last 12 months? Do you think it’s hard to find work in town? 3. |

4. What would you rather purchase a new build property or a pre-owned property with may require general upgrading? |

5. Are the three main priorities to buying your first property? |

6. What are your three concerns when looking to buy? |

7. Are you aware of the help to buy government scheme for first-time buyers? |

8. If yes, would you consider the help to buy scheme, if so please give reasons? |

9. What areas do you think are in demand in Hartlepool? |

10. What style of properties do you think first time buyers are wanting? |

11. The new mortgage calculator is a helpful tool to analyze the risk of property purchase, have you ever used it? |

12. What do you think of the stamp duty change? |

13. In recent months banks have reduced their borrowing some of the big names like Barclays and Santander have reduced borrowing from as much as 5.5% to 4.5% how do you feel this will affect first time buyers? |

14. How did you find it obtaining a mortgage as a first-time buyer? |

15. From April 2014 an affordability calculator was launched which assesses the person outgoings, what are your thoughts on this when applying for a mortgage? |

The results of the interviews showed that the first time buyers were inclined to purchase properties in the area of Hartlepool, as they had had permanent employment in this district. While discussing the employment opportunities in the area, many of the interviewees indicated that the conditions are getting better slowly. As one respondent quoted;

“I am looking for a property in Hartlepool as I work nearby and have a family. As per my understanding of the area, you can get a good job if you have skills and are educated. Better than the recession period to say the least, when all we used to hear is the so many people have been fired”.

(Hartlepool resident and first-time buyer, yet to secure a property)

While discussing the Hartlepool’s demographic factors, the majority of the participants suggested that the area in need of developments, and the market is relatively slow, especially with the regards to refurbishment properties. It was also observed during the discussions that there is a lack of confidence in the first time buyers concerning the housing market of Hartlepool, as they believed that that the area is still getting out of a recession period.

“Hartlepool people think the housing market is increasing and when you go out to evaluate properties they present it as it’s worth more than it is... due to the press and papers basically saying houses are now increasing, maybe down south but not necessarily here. But actually, Hartlepool is still just coming out the recession”

(Hartlepool resident who have secured a property)

On the discussion related to the most important requirements and needs of the Hartlepool first time buyers, it was observed that most of the participants were inclined to say that financial aspects are the most important concern. As one of the participants quoted;

I think finance is what matters in the end. If the market remains stable, I won’t be losing money…however you just never know. Purchasing property is a big step and you have to consider various aspect. How much we will be paying, is the property meet my demands, my future need etc…”

On the discussion related to the government schemes such as Help to buy, one respondent quoted;

Well I think it is affected the new build market more than used housing stocks, they are the odd first-time buyers who are wanting to secure housing through help to buy… but erm… they seem to not know that you can do it as much”

Other interviewees also suggested that this a good scheme, however it may not be the ultimate solution to develop this market (referring to Hartlepool) since the majority of the dwellings are refurbishment properties. One responded also raised concerns over the security of jobs in terms of their temporary nature of job contract and its negative impact on obtaining support from mortgage lenders. The respondents also agreed that a new mortgage calculator is a helpful tool, however, some of them had rarely used this application as they utilized services of financial consultants from lenders.

Regarding the priority of the first time buyers with respect to the dwelling types, the majority of the participants indicated that they would like to move to new build houses.

“New build housing probably suits me more, I don’t have time for the stress of older houses, my parents have an older house and the upkeep would cost a lot. New builds for me”

During the discussions, it was observed that the first time buyers had different prioritize. One of the participants preferred the area of Westfield and indicated they would purchase a new property in this area, while others suggested that they did not want to spend on house renovations and they want the houses as per their family preferences, such as 3 bedroom houses, large kitchen, storage spaces, parking area etc. Another respondent added;

“I would say… 3-bed housing in the area of Hart, see two-bed houses aren't really practical because if you ever want children of just more space you know you're going to have to move or extend so it is easier to get a three ned house then you don’t need to think of moving”

Regarding the demand and supply factors, and the overall housing market of Hartlepool, majority of the respondents suggested that there have not been any dramatic falls in the market, so they feel at relative ease. One participant highlighted that the three are various types of dwellings available in the market, some which get sold quickly, and some which are difficult to sell, as it depends upon the structure of properties, budget and the locality of the dwelling. One respondent added;

“Dwellings are available, YES, but are these up to my requirements, NO…if you ask my prospective, a balance has to maintain between priorities of the client, the budget and the area. I have been in touch with various agents, but I am yet to find a property that best suits me.”

These results implicated that there are indeed shortages of dwellings concerning the specific first-time user needs. To gain further information from an experienced and expert source, an interview was also conducted with a representative of ‘Bellway Homes’, one of the leading developers in Hartlepool, who are currently developing Bishop Cuthbert in the North of Hartlepool. This construction programme near Hart Village includes a series of 2 to 4 new bed semi houses with garage.

When asked about the development initiative and whether there is a demand for such houses, the participant suggested that there is a definite need of new contemporary houses, as the living standards/style have now changed as compare to early years of 20th century. Smaller 3 bedroom semi houses with an integral garage and garden turfed, carpets and stamp duty are in high demand, and the sale has now started to increase as the developments are getting into the final stages.

“Back when I first started with Bellway, the types of housing where 5-bed houses with double garages and study's and utility rooms were in demand, now buyers are wanting huge kitchens and extra living spaces... The first-timers are wanting practical spaces and storage, you know garages aren't as important now. Some of the house styles don’t have garages”

To a question related to the financial benefit of moving to a renovation property rather a new construct, the participant stated;

“I don’t think people are too bothered, because houses are going to go up aren't they, and with help to buy if you pay off the loan you got an extra 20% of the house so you’re kind of building up your money”.

This statement indicated the impact of help to buy schemes, as many clients would rather buy a newly built property through a secured lending process as an additional advantage, and there has been an increased market of new build houses now. Although they went on to add that old dwelling are also demanded by the investors looking to get a good bargain. When asked about the impact of help to buy scheme, their response was;

“It's literally taken us by storm... at first it was pretty slow I think people didn't really grasp it, I think people thought it was a huge equity loan what has massive amounts of interested added but it really is working to our advantage now .. Overall, I don’t know the exact figures mind, but a lot of sales here are through the help to buy. I would say most of our buyers are youngish some are older but are moving from smaller houses and using the help to buy when needs must…it's a great package I would even use it

The respondent further added;

“I don't think it is creating a false economy mind (I think that’s negative attitude), it is helping first-time buyers get on the property ladder which is hard especially with the market not massively dropping, even in a recession the prices weren't as low, probably due to the housing shortage”

To a question related to first time buyers, the responded suggested that the first time buyers are more concerned with their financial conditions, as the increasing market prices may well put them at a higher risk. They also confirmed that they do often see client which have limited lending and are unable to secure a deal.

Sustainable Supply Chain Risk Management

While discussing the effects of the latest stamp duty changes, the participant agreed that these changes are helping the young buyers as the process has much improved now. They further suggested that this change may actually help many residents who wanted to move early but couldn’t due to price limit implications.

The participant further pointed out that the Hartlepool market has started to grow after recession and Bellway has plans to build further larger sized properties which are to be specifically designed for family use.

4.2.2 Questionnaires

To achieve the objectives of this research; that is investigating the factors closely associated with the first time buyers and their response, a tailored questionnaire led by the 26 questions were filled by the potential first buyers in the locality of Hartlepool. The detailed form of questionnaire form has been documented in Appendix 1 of this paper.

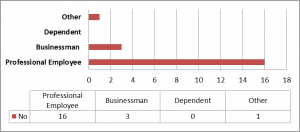

In response to the question related to the profession of the potential first buyer clients, the following response was received;

Figure 12; Response of fist buyers on the profession

As indicated from the table above, 16 out of 20 clients who were to looking to purchase property in the Hartlepool were professional employees. Majority of these clients were also working in the Hartlepool sub-areas, as indicated by the response received on the question of “Do you live/work in Hartlepool?” however some participants commute.

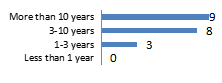

In response to the questions relating to livability in the area of Hartlepool, the following response was received;

Table 2; Results (livability)

Inquiry |

Results (Response out of 20) |

| have you lived in Hartlepool area for |  |

| Describe this area as |  |

| The employment rate in Hartlepool has |  |

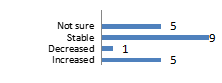

As an indicated form the results, a higher proportion of participants had lived in Hartlepool for more than 10 years. The response further suggested that according to the opinion of potential first buyers, the employment rates in the area of Hartlepool has remained stable, whereas 5 out of 20 participants indicate that it may have increased or they were not sure. Furthermore, more than 50% of the participants agreed that the area needs further development to enhance the standard housing market

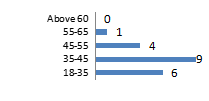

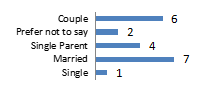

To gain information on the characteristics of the first users, questions related to their age, marital status and dependents/children were included, the results of which are as below;

Table 3; Results (client characteristics)

Inquiry |

Results (Response out of 20) |

| Age range |  |

| Status |  |

| Dependents |  |

The results show that 15 out of 20 clients of age less than 45 years, showcasing that a lot of young and mature employees were the potential first buyers. Moreover, only one of the client were single and 60% of the clients had dependents. This implicates that first buyers were either married/cohabiting, living as a couple, or were single parents looking to purchase property for their families.

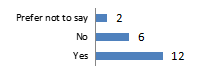

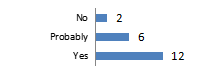

The majority of the clients were currently living in rented accommodations, with the rent ranging between 400 to 1000 pounds, and they were only somewhat satisfied with the quality of the accommodation. Furthermore, the major proportion of the participants suggested that they wish to purchase the property in the Hartlepool sub-areas, as they were living and/or working in this area. In response, the question related to the self-sufficiency of housing in the subject area, more than 60% indicated that the area is definitely or at least probably self-sufficient, whereas the remaining answered that they were not sure or it is not self-contained market area.

In response to the question related to the dwelling type preferences, the following response was received;

Figure 13; Response of fist buyers on Dwelling preferences

As it can be reviewed from the graph above, the majority of the clients wanted to move to a house (more than 80%), preferably that is detached. Some of the participants also indicated their preferences in terms of the number of bedrooms, suggesting that they needed at least three bedrooms (larger sized), more storage space and en-suite bathrooms in their preferred house Many of the respondents further indicated that they would not purchase the property until unless the dwelling meets their preferences.

Development of Sustainable Homes Through Renewable Energy Sources

In order to receive feedback on new and dwellings in terms of first buyer preferences, and their opening on the old dwellings, three specific questions were incorporated in the questionnaire form, the results of which are as follows;

Table 4; Results (preferences)

Inquiry |

Results (Response out of 20) |

| Prefer to purchase New-build properties |  |

| Existing/old dwellings in this area are |  |

| Clients may not prefer to purchase old dwellings because |  |

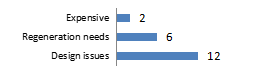

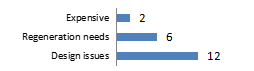

As shown in the results above, the majority of the clients preferred to move to a new house or suggested that they may consider both types of dwellings (old and new), depending on the offer. According to the results, the majority of the clients believed that the old dwellings were of poor quality and were not designed for their preferred requirements, and some of them also needed re-generation. Only 10% of the clients considered the old dwellings as expensive.

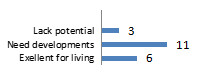

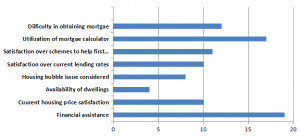

In order to obtain the first buyer views on the economic as well supply and demand factors, various sets of questions were included, the results of which have been documented as below in summarized from;

Table 5; Results (summary)

As it can be reviewed from the table above, almost all the first time buyers had consensus on the point that it is not possible to purchase suitable housing without financial assistance. 60 % of the participants suggested that they are somewhat satisfied with the current pricing in the area of Hartlepool, which could be due to the fact that the prices have remained stable for the last many years, and compared to other areas of the UK, the house prices are relatively low. On the question related to the demand of housing, 60% suggested that sufficient dwellings meeting their demands are ‘not available’ in the market, whereas the rest of the participant either confirmed that there are sufficient dwellings or these were probably there but they were yet to visit these facilities. This suggestion could be further linked with the perspective of the clients and their experiences of the Hartlepool marker survey.

Another important point was the consideration of factors such as the housing bubble when considering to purchase a property. Most of the participants (12 out of 20) suggested that the housing bubble is not a definite concern. However, 40% if the client agreed that this probably influences their decision in purchasing a property. This could be because of the fact the purchasing any property involves huge sums of cash, and any variation in the market could potentially damage the financial standing of the clients. Since the majority of the clients had families and were full-time employees, this was probably one of the most critical financial decision they had to make. From another perspective, the increasing expectation of profits from property purchase could well have been the reason behind this client’s considerations

As discussed in the desk-based research, the reduced interest has stabilized the housing market in most areas of the UK. On the question relating to whether they are satisfied with the current UK lending rates and government’s efforts/scheme to support the first time buyers, majority of the respondents confirmed that the situation has indeed improved as they were ‘somewhat satisfied’ with the interest rates and government schemes such as ‘help to buy’ as they were specifically tailored for encouraging the actual residential property buyers and not the investors. It is also important to note that the recent decline in interest rates might have influenced the first buyers participating in this research. Moreover, the majority of the clients agreed that mortgage calculation is indeed a helpful tool, however, 65% of the participants suggested that obtaining a mortgage is difficult in today’s tight economic situation.

Chapter – 5; Discussion & Recommendations

The starting point for analyzing any housing market is estimating the new housing rates in comparison with the previous year’s rates. This historical information was obtained from the Department for Communities and Local Government (DCLG). Apart from this, data were also obtained on a sub-regional level from Tees Valley Unlimited. The history of Hartlepool housing market suggested that it has remained stable in the last few years, as it has still not completely recovered from the recession period. It was also observed during this research that there is an increased demand for new builds, as there have been various approved developments programs such as by Taylor Wimpy and Bellway Homes, with many other development programs not approved due to traffic and flooding concerns. The prices of the houses have also decreased for the clients, and are now much in the range of the new buyers through the help to buy schemes.

It was important to note that the viability of the house prices can also be observed from the correlation between mortgage rates, given out by companies and banks, and the average household income of the people. If the people are unable to pay their monthly mortgage rates, then this will result in defaulting on their payment and ultimately losing their property. If such a thing happens to a large proportion of people, then they will go out in the market for the sake of selling their property which will bring the prices down because of more supply than demand of houses.

However, the mortgage rates have now been at their lowest since 2008, and the amount of income that is spent on repaying the mortgage is heavily dependent on the interest rate. The low-interest rates can have two counterbalancing effects on mortgage payment. It is true that the low-interest rates will mean that the borrower will have to pay back comparatively lesser money but they may be tempted to borrow more money thus having to pay larger sums as interest. This was specifically noted from the results obtained from Homes and Communities Agency’s report of 2015, which stated that the number of first buyers in the year 2014 has decreased however the total mortgage lending amounts have increased. If the interest rates increase in correspondence to the increase in house prices, then it may become difficult for debtors to pay back their interests. Thus, repossessions and rising arrears increase in that period. However, as observed through this research, the help to buy schemes has definitely influenced that market of Hartlepool, as evident from the new development programs and from views obtained of market experts and the actual first-time buyers.

It was observed in the literature review that the people of Borough have also been affected by the recession in the economy. The percentage of people that are going through the challenges of mortgage payment in Hartlepool and potential repossession had increased during the recession period, according to TVSHMA, 2012. However, reviewing the yearly income of the residents of Hartlepool, unemployment rates and other economic factors in comparison with other districts, it can be suggested that the district is recovering well, which may have consequently resulted in an increased interest of new buyers in the market.

The most important findings of this research through Interviews, questionnaire and literature reviews (ONS, 2012; TVSHMA, 2012) which are deemed to be highlighted are;

- The people of Hartlepool tend to stay in Borough

- The median house price in Hartlepool in the year 2011 was £110,000, which is less than the national average

- Dwelling in this district are more affordable as compared to other areas, as the house prices to earning ration are relatively low

- The suburbs in west and south are comparatively rich

- The new governmental schemes are extremely supportive to first buyers. The interest rates are at the lowest.

- The demand for private residence here is strong

- The area is need of further developments, and refurbishments of dwellings, as the older dwellings, are considered to be not satisfactory for many potential clients

- The market demand here is found to be greater for new builds.

- The new housing market has been established at Hart village (north), Marina (central) and Middle Warren (northwest).

- Majority of the first time buyers are having difficulty in finding an appropriate residence.

- The new developments have started to increase

- The total amount of households are approximately 40,000.

- Its population is 92,600 and it will reach to 97,400 by the end of 2037

The summarized results presented above indicate that the area of Hartlepool is economically as well as demographically viable for the potential growth of the housing market. The residential incomes, employment rates, mortgage rates, house prices, development programs/policies, trends and the needs / prioritize of the first time buyers presented in the previous sections also suggest that the market is expected to grow in prospective future, especially when considering the impact of lower mortgage rates and help to buy schemes and their influence on the first time buyers. The same pattern of observations was noticed during the conducted interviews and through the questionnaire results.

Furthermore, the data obtained with respect to the available dwellings in this district suggested that market is more or less in balance, but facts demonstrated above highlight that there might be a probable imbalance between the demand and supply, especially with reference to availably of stocks that meet the new entrants into the market. There is a high demand for new builds, and somewhat of the old dwelling due to their lower prices in the potential first clients. The civil society has moved on, and there is a definite need to consider this shift in trends of housing needs when planning for future residential developments

These facts were further observed in the report Hartlepool Borough Council, 2014, where they presented the Future Housing Provision in Borough for the next 15 years. The incoming Local Development Framework (LDF) can be guided by the help of the Housing Strategy. It is expected that the current Hartlepool Local Plan will be replaced by LDF. According to this report, the main plan is to assign areas for houses, jobs, construction and in Borough. This strategy will be able to replace the policies that were established in the Local Plan. The objective of the Core Strategy is to proceed with the HMR plan, devise a way to construct 4800 new dwellings for the next 15 years. This is because it is predicted that in future, there will be a need of more houses, due to current economic and demographic factors and expected rise in population, and the current housing system will fail to accommodate everyone. This is why there is a dire need to make changes and improve the housing structure.

There are many issues in Hartlepool housing market which need to be resolved through this strategy. This can be accomplished by coordinating with the demands and needs of people. The main principle for a housing strategy is to sustain the communities and implementing a policy for maintaining a community. This must ensure that the needs of people are considered, which includes high-quality design (which must incorporate client preferences of today’s market), low-priced houses, and considerations of sustainability. The location apart from cost for housing system is also important. Along with the Core Strategy, a community must also be involved in assigning land for the next 15 years.

Hartlepool has to deal with issues of financing and lack of space. The land for new housing schemes are insufficient, probably due to flooding and traffics concerns of the future. However, these weaknesses of the local housing market have not prevented Borough to build additional houses around 300 per year. This has been possible due to public sector financing that also supports private progress. The Housing Strategy must also intend to solve these issues and plan new constructions at a larger scale, with additional focus on facilities and health opportunities as well as the economy. They have to be responsive to the newly approved sites. A link has to be established between the employment and transfer of wealth creators and new houses.

Housing affordability means to own houses at a price which is very reasonable for the first time buyers and can be afforded in a market for permanent ownership. The most important way for making sure that affordable houses can be purchased in future is to make a planning obligation. Houses that are affordable should be included in the Core strategy, with the aim to secure a considerable proportion of on-site houses that can be afforded as part of all private housing development. The amount of supply depends on the economic practicality of private schemes and other factors that have been much discussed in this research. An off-site contribution is required for executive housing sites. For new houses that are affordable, the service charges should be kept minimum.