The Impact of Technology in Improving Resilience and Sustainability in Construction Projects – Case of BIM and LCA

February 4, 2021

CEM 204 International Construction

February 5, 2021

Executive Summary

The first section of the paper (Part A) highlights the ‘lean’ concepts in modern manufacturing. The following 4 fundamental concepts have bene covered in this approach, which details how these concepts provide support in improving the quality and efficient in manufacturing industry

The second section of this coursework (Part B) answers 5 different analytical questions which are related to the economics, quality and organizational aspects of the manufacturing industry.

Part A

“Lean” Manufacture

The concept of lean manufacturing was first presented by Toyota Production Systems (TPS), which laid the foundation of methods which can be adopted to minimize the waste of manufacturing processes (Herron et al., 2008). In today’s manufacturing industry, lean production can be described as the multi-dimensional and integrated system of management practices that has the potential to systematically enhance the quality as well as efficiency of manufacturing (Shah et al., 2003).

The research conducted by Yadav et al in the year 2010 presented various fundamental lean principles, such as;

- Standardization of production procedures; to enhance system efficiency and quality

- Integrated coordination; to share information and ensure communication between the teams

- Generation specified simple and logical pathways for production

- Continues improvement for optimization of activities etc.

Successful implementation of such lean principles in production environment can lead to cost reduction, increased productivity / efficiency, timely performance delivery and optimum manage for any organization; as evidently discussed in Piercy and Rich (2009).

Just In Time

During the manufacturing process, and activity that increases the cost without having to increase the worth of the product can be considered as waste. These activities may include unnecessary movements of stocks / materials, accumulation of additional / abundant stocks and un-optimized production system/method that may require re-working in the production process line. The just in time approach minimized such wastes and enhances the quality and efficiency of production by;

- Optimizing the stock levels and minimizing unnecessary movements of stocks

- Improving the quality of items

- Minimizing production variability

- Minimizing production times as well as lead times of delivery

- Reducing various expenses in manufacturing process

Therefore, just in time strategy helps in increasing the efficiency of production by attempting to utilize the most of the available resources and by using specifically engineering time scales / schedules. The eventually helps in reducing expansive inventories, long production times, eliminating production of defected items, ensuring delivery times are met (Wright, 2001).

Total Quality Management

The total quality management is an administrative concept that has the potential to enhance the performance of production. This approach requires the complete organization to assume responsibility to ensure quality of the products and the services by continuously improving the effectiveness of all the stages of the operational processes. This implies to quality management from the production stage to finished product; incorporating its effectiveness of all the teams of the manufacturing process. It also incorporates quality control practices as well as administration of the personnel involved (Yadav et al., 2010).

The fundamental idea of quality management may have bene derived from product assessment (quality checks) prospective, but over the years it has also evolved / transformed to address process control parameters, process optimizations, use of statistics and persistent changes and quality functional deployment. The efforts undertaken in total quality management therefore results in quality and efficiency enhancements throughout all the stages of the manufacturing (Papadopoulou and Ozbayrak, 2005).

Total Productivity Maintenance

The total productivity maintenance can be described as a systems that enables independent / self-sufficient maintenance of assets of an organization; primarily the machinery involved in the manufacturing purpose. This is normally undertaken by utilizing the skill sets of expert labour/operators and other technical resources. The total productivity maintenance is fundamental concept that can ensure delivery of optimum yields through keeping the ‘required working conditions’ under control. This implies that plant/equipment operators undertake regular / schedules maintenance of the equipment, while the management ensures that the specific procedures are followed in accordance with standard operations and maintenance procedures. It also ensures that predictive as well as preventive maintenances checks are regularly completed.

Another aspect of the productivity maintenance is the utilization of simple but most effective equipment, to ensure that highest quality products are produced at shorter time, costs and at lower maintenance. This strategy implicates that the choice of equipment must be based on these considerations, and potential enhancements in hardware must be considered in light of the parameters such as reliability, technology and economic viability. This practice consequently results in improved quality and efficiency of manufacturing (Sullivan et al., 2002)

Part B

Question B1.

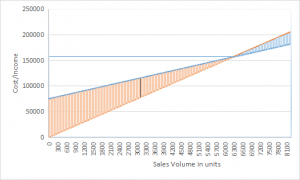

The Machine A sell the products for £25 per product, with variable cost per product produced is £13, and total fixed costs of £75,000. The break-even graphs (Costs/Income -v- No of Products) for Machine A can be produced as;

The plotted graph shows that the Machine A’s breakeven point occurs when the company sells approximately 6300 units, and at the point when the Cost/income researches about £157,000

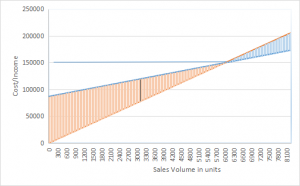

Similarly, the Machine B sell the products for £25 per product, with variable cost per product produced is £10.50, and total fixed costs of £87,000. The break-even graphs (Costs/Income -v- No of Products) for Machine B can be produced as;

The plotted graph shows that the Machine B’s breakeven point occurs when the company sells approximately 6000 units, and at the point when the Cost/income researches about £150,000

These analyses show that the although machine B’s capital costs is more than machine A, but due to its reduced variable cost, the company will reach the breakeven point at ‘lower total costs’ and by ‘selling fewer amount of products’. Therefore, Machine B is recommended for purchase.

Question B2

Total components in batch = 2500

Material cost of each component = £2

Therefore, total material cost of batch = £5,000 (2500 x 2)

Time required for each component = 4 minutes

Time required for complete batch manufacturing = 10,000 minutes (2500 x 4)

Cost of operator = £15 per hour = 15/60 per minute = £0.25 per minute

Total direct labour cost of each batch = £0.25 x 10,000 = £2500

Total over heads of the company = 350% of total direct labour cost = 350/100 x 2500 = £8750

Therefore, the total cost of batch is the sum of total over heads, total direct labour cost and total material cost = 8750 +2500 + 5000 = £16,250

So, the true cost of manufacturing each component = 16250/2500 = £6.5 per product

Question B3

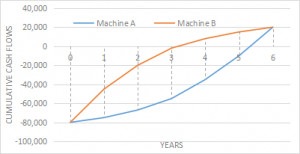

(a)(i): For machine A, cumulative cash flow can be determined as;

Year | Cash Flow (£) | Cumulative Cash Flow (£) |

0 | -80,000 | -80,000 |

1 | 5,000 | -75,000 |

2 | 8,000 | -67,000 |

3 | 12,000 | -55,000 |

4 | 20,000 | -35,000 |

5 | 25,000 | -10,000 |

6 | 30,000 | +20,000 |

Therefore, payback period = 5 + (10/30) = 5.33 years

Similarly, or Machine B;

Year | Cash Flow (£) | Cumulative Cash Flow (£) |

0 | -80,000 | -80,000 |

1 | 35,000 | -45,000 |

2 | 25,000 | -20,000 |

3 | 18,000 | -2,000 |

4 | 10,000 | +8,000 |

5 | 7,000 | +15,000 |

6 | 5,000 | +20,000 |

Therefore, payback period = 3 + (2/10) = 3.2 years

Based on the payback analyses, it can be reviewed that the machine B’s payback period, which is 3.2 years, is much shorter as compared to Machine A’s payback period of 5.33 years. This suggest that the machine B can be chosen for the purchase as it justifies a quicker return on investments.

(ii): However, the trend of cash flows indicate that the machine A can be more profitable in the prospective future, as it showing an increasing growth in profits, illustrated in the graph below;

Therefore, purchase of Machine A can be justified considering this higher cash flow growth rates of machine A

(b): For machine A;

Year | 1 | 2 | 3 | 4 | 5 | 6 |

Real Cash Flows (£) | 5000 | 8000 | 12000 | 20000 | 25000 | 30000 |

Yearly discount factors at 7% | 0.9346 | 0.8374 | 0.8163 | 0.7629 | 0.7130 | 0.6663 |

PV cash flows (£) | 4673 | 6700 | 9795 | 15258 | 17825 | 19989 |

From the table above, the total PV cash flow, accumulative of 6 years = £74, 240

Therefore, NPV (Net present value) can be calculated as = 74,240 – 80,000 = £ -5,760

Similarly for Machine B,

Year | 1 | 2 | 3 | 4 | 5 | 6 |

Real Cash Flows (£) | 35000 | 25000 | 18000 | 10000 | 7000 | 5000 |

Yearly discount factors at 7% | 0.9346 | 0.8374 | 0.8163 | 0.7629 | 0.7130 | 0.6663 |

PV cash flows (£) | 32711 | 20935 | 14693 | 7692 | 4991 | 3331 |

Total PV cash flow, accumulative of 6 years = £84, 353

Therefore, NPV (Net present value) can be calculated as = 84,353 – 80,000 = £ 4,353

(c): Now considering the discount (inflation) rate of 4% for each year of the project, the following PV cash flows are obtained;

Year | 1 | 2 | 3 | 4 | 5 | 6 |

Real Cash Flows (£) | 5000 | 8000 | 12000 | 20000 | 25000 | 30000 |

Yearly discount factors at 4% | 0.9615 | 0.9246 | 0.8890 | 0.8548 | 0.8219 | 0.7903 |

PV cash flows (£) | 4807 | 7396 | 10668 | 17096 | 20547 | 23709 |

Total PV cash flow, accumulative of 6 years = £84, 223

Therefore, NPV (Net present value) can be calculated as = 84,223 – 80,000 = £ 4,223

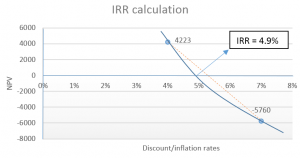

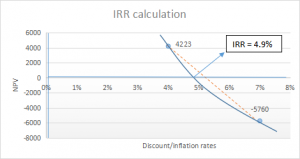

The Inter Rate of Return (IRR) is calculated by drawing the NPV values against the discount (inflation) rates; as IRR is the rate at which NPV becomes zero. Therefore, IRR for machine A over the 6 years periods is calculated by a graphical methods using the NPVs for discount rates of 7& and 4%

Therefore, the IRR = 4.9%

Question B4

(a): The average and range for each sample batch is calculated in the table below;

| Batch 1 | Batch 2 | Batch 3 | Batch 4 | Batch 5 | Batch 6 | Batch 7 | Batch 8 |

| 25 | 25.2 | 25 | 25.2 | 25.3 | 25.2 | 25.4 | 25.7 |

| 25.1 | 24.9 | 25.1 | 25.4 | 25.4 | 25.4 | 25.5 | 25.6 |

| 24.8 | 24.9 | 25.2 | 25.4 | 25.3 | 25.3 | 25.6 | 25.7 |

| 25.1 | 25 | 25.2 | 25.5 | 25.5 | 25.6 | 25.7 | 25.6 |

| 25.1 | 25 | 25.3 | 25.4 | 25.6 | 25.6 | 25.6 | 25.6 |

| 24.9 | 25.1 | 25.1 | 25.5 | 25.2 | 25.5 | 25.6 | 25.6 |

| 25 | 25.1 | 25 | 25.3 | 25.3 | 25.6 | 25.7 | 25.4 |

| 25 | 24.9 | 25.4 | 25.2 | 25.5 | 25.6 | 25.6 | 25.7 |

| 24.9 | 25.1 | 25 | 25.2 | 25.5 | 25.4 | 25.7 | 25.6 |

| 25.1 | 25.1 | 25.1 | 25.4 | 25.4 | 25.4 | 25.4 | 25.8 |

Average (cm) | 25 | 25.03 | 25.14 | 25.35 | 25.4 | 25.46 | 25.58 | 25.63 |

Range | 0.3 | 0.3 | 0.4 | 0.3 | 0.4 | 0.4 | 0.3 | 0.4 |

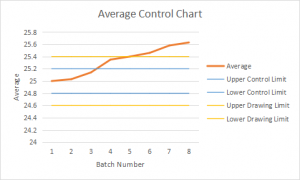

(b): The average control chart is plotted for all 8 samples batches;

And the range control charts is plotted as follows, showing the appropriate limits;

(c): Analyzing the data of PVC pipe diameters, it can be observed that the average diameter of first three batch samples are within the defined control limits of 25.0 +/- 0.2 cm. The positive increase in the average diameters of the sample batches than reaches the upper drawing limits at batch number 5. This implicates that the batch number 5-8 are beyond the drawing specifications and must be rejected, as they do not meet the required quality/specification standards.

However, the range control charts shows that all the batches produced are within the defined range of diameters, as the pipe sized do not exceed that the control limit (5mm) and the action limit (8mm) within a batch. This shows that production of pipes in in a batch are in accordance with the set/target range parameters, but this does not implicate that the sizes are in accordance with the drawing specifications.

Analyzing both the trends, it can be concluded that there is not much variations in the range of the pipe diameters in each batch, however the average diameters are not in compliance with the drawing specification requirements. The increasing diameters trend of pipe manufacturing was observed in the calculations, and this issue needs to be adjusted/controlled to ensure standardized quality of the products

Question B5

The equation of Economies of Scale is given as;

C2 = C1 x (Q2 /Q1) n

C1 (Original manufacturing project cost) = £1,034,564

n = 0.6, and

Q2/Q2= 3 (new manufacturing project is 3 times the size of original project size)

Replacing the values gives;

C2 = C1 x (Q2 /Q1) n

C2 = 1,034,564 x (3) 0.6 = £2,000,000

Therefore, the new manufacturing project would cost £2,000,000.

References

Herron, C. and Christian, H. (2008), The transfer of selected lean manufacturing techniques from Japanese automotive manufacturing into general manufacturing (UK) through change agents, Robotics and Computer-Integrated Manufacturing, 24, pp.524-531

Piercy, N. and Rich, N. (2009), Lean transformation in the pure service environment: the case of the call service center, International Journal of Operations & Production Management, Vol. 29, No. 1, pp. 54-75.

Papadopoulou, T. C. and Ozbayrak, M. (2005), Leanness: experiences from the journey to date, Journal of Manufacturing Technology Management, Vol. 16 No. 7, pp. 784-807

Shah, R. and Ward, P. T. (2003), Lean manufacturing: context, practice bundles, and performance, Journal of Operations Management, 21, pp. 129–149

Sullivan, W. G., McDonald, T. N. and Van Aken, E. M. (2002), Equipment replacement decisions and lean manufacturing, Vol. 18, pp. 255-265

Wright M. (2001). What Should Students Learn about Manufacturing?” Technology and Children, Volume 5, Issue 3, p. 2-3.

Womack, J.P. and Jones, D.T., 1996, Lean Thinking: Banish Waste and Create Wealth in Your Corporation

Yadav, O. P., Nepal, B., Goel, P. S., Jain, R. and Mohanty, R. P. (2010), Insights and learnings from lean manufacturing implementation practices, Int. J. Services and Operations Management, Vol. 6, pp. 398-422.

Get 3+ Free Dissertation Topics within 24 hours?